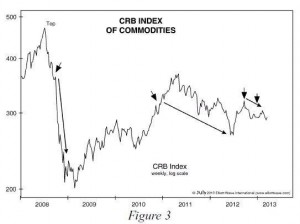

Traditional wisdom tells us that when the money supply expands the price of commodities rises. Today Robert Prechter takes a look at what has actually happened to commodity prices since 2008 during a period when theoretically the FED has been pumping up the money supply. ~Tim McMahon, editor Commodities Falling Despite QE: What Does That Mean? Robert Prechter: "Charts tell the truth. Let's look at some charts." By Elliott Wave International During QE3, the latest round of the Fed's quantitative easing, the stock market rose. We all know that. But did you also know that commodities fell? That's right: QE3 had zero effect on commodities -- or maybe even a negative effect. In … [Read more...]

Quantitative Easing

In early 2001 Japan implemented the first instance of quantitative easing although for many years prior to 2001 the BOJ (Bank of Japan) had claimed that quantitative easing was not effective in fighting deflation and therefore had rejected its use. But in response to the liquidity crisis beginning in 2007 the United States followed suit and began QE1 which was then followed by QE2 and QE3..

Quantitative Easing - Q&A

Q: What is Quantitative Easing?

A: Quantitative Easing (Q.E.) is when the Federal Reserve buys Treasury obligations (T-Bills, T-Bonds and -Notes) from the member banks. Generally the sale is handled at an "auction" for the banks by "primary dealers" like Morgan Stanley.

Q: Is Quantitative Easing the same as "Printing Money"?

A: No. Although they are similar they have one key difference. In a normal inflationary "money printing" scenario the FED buys Treasury obligations directly from the Treasury. In so doing, it increases the money supply. Basically it is an accounting gimmick that allows the U.S. Treasury to create more debt thus expanding the money supply. But with Q.E. the debt has already been created and is already sitting on the books of the banks. So the FED takes it off the banks hands and gives them cash instead. (Actually, the FED just credits the numbers to the Bank's account, it doesn't actually move any currency). But this process just trades one type of asset (Treasury's) for another (cash deposits). It doesn't involve creating any new Treasury debt.

Q: Where does the FED get the money to pay the banks for Quantitative Easing?

A: It uses the reserves on its balance sheet. These are deposits from the member banks.

Q: So if it is just moving assets around why does the FED do it?

A: When the Treasury obligations are held by the member banks they can't be loaned out to borrowers. In a "liquidity crunch" the banks need cash not debt obligations to pay their bills and to loan to borrowers. The FED doesn't need cash so it can hold the debts and the member banks can make more loans. Theoretically, this increases money in circulation (as long as the banks actually loan the money out).

Q: Does Quantitative Easing have any effect on interest rates?

A: Yes, by buying Treasury Bills the FED is driving interest rates down. When the demand for T-Bills is up it drives the interest rates down because the bidding is based on who is willing to accept the lowest interest rate. More bidders = lower interest paid. Many other rates are affected by the lower T-bill rate so it drives all interest rates down making it cheaper to borrow money.

Q: Does the FED make money on the Treasury Bills it owns?

A: Yes, it earns interest on any T-Bills it owns just like any other T-Bill holder but according to Ray Stone, a former Fed insider and founder of Princeton based Stone McCarthy Research Associates, the FED actually returns the money to the Treasury. Last year the Fed earned about $90 billion in profits, compared with about $30 billion in years prior to the bond purchases. This benefits taxpayers by actually reducing the deficit.

The Effects of Quantitative Easing

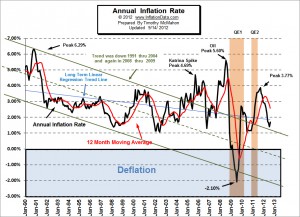

Quantitative Easing Effects- You have probably heard that the massive inflation of the money supply through Quantitative Easing is going to result in hyperinflation or at least massive inflation. But so far that hasn't happened. As a matter of fact since the end of QE2 in June of 2011 inflation rates have fallen from 3.63% in July 2011 to 1.41% in July 2012. How is that possible? The first reason is that the FED is playing a game with the banks. The FED loans money to the Banks at nearly Zero percent interest the Banks turn around and loan the money to the Government at 3% interest to finance the deficit. This gives the banks plenty of profit to shore up their sagging balance sheets. But … [Read more...]

What is Quantitative Easing?

Is Quantitative Easing Money Printing? Quantitative Easing is often referred to as "money printing" or a way for the government to increase the money supply. According to Wikipedia, quantitative easing is different from the typical method whereby governments buy treasury debt to increase the money supply. In QE1 when the market was panicked, and banks didn't want to buy government bonds, the central bank implemented "quantitative easing" by purchasing relatively worthless financial assets (like mortgage backed securities) from banks and giving them new electronically created money. So this is straight forward money printing compared to the more round about traditional method. Thus … [Read more...]

Fed To ‘Hold Off’ On QE 3

We noted extreme levels of optimism earlier today. What could possibly trigger a correction in stocks and commodities? If the Fed fails to signal and/or announce another round of quantitative easing (QE), it would undoubtedly leave the markets disappointed. The Fed uses the Wall Street Journal (WSJ) as a medium to communicate with the markets. It is possible someone at the Fed picked up the phone and said, “We need to temper short-term expectations for another round of QE. Can you help us out?” Friday’s WSJ has an article titled “Fed Holds Off For Now on Bond Buys”. Notice the word “may” is not included. Here is the first paragraph of the article: Federal Reserve officials are waiting … [Read more...]

Why Quantitative Easing Has NOT Brought Back Inflation

When the FED began quantitative easing to halt the deflationary crash of 2008, almost everyone was convinced that it would result in massive inflation. The lone voice proclaiming that it wouldn't stop the deflationary express train wreck was Robert Prechter. In the following article Prechter explains why inflation never materialized. It is an excerpt from Prechter's, Independent Investor eBook 2011. I hope you enjoy this short excerpt. See below for details on how to get the eBook in its entirety for free. ~ Tim McMahon, editor … [Read more...]