The current round of massive Corona Virus easing began Monday March 16th, 2020, with the FED buying $40 billion in Treasuries and then buying another $50 billion in Treasuries on Tuesday. By Thursday morning, it had upped the plan to $75 billion PER DAY and added $10 billion in mortgage securities. By Friday morning, the Fed had decided to buy $107 billion worth of Treasuries and mortgage-backed securities. In its first week, the FED purchased $317 billion worth of assets, which is slightly faster than the Fed balance sheet grew at the height of the 2008-2009 financial crisis. Initially, the Federal Reserve estimated purchases of $500 billion but FED chief Jerome Powell said the initial estimate was a floor and he emphasized that there was no ceiling.

The European Central Bank has announced its own quantitative easing program. The ECB originally announced that it intended to buy 750 billion euros ($819 billion) worth of bonds but the ECB said it will increase purchases as needed.

With money printing on that scale, many people are wondering if it will cause massive inflation or even hyperinflation.

What is Inflation and What Causes it?

When talking about inflation most people think of an increase in the price that they pay for goods and services. Technically, that is called “Price Inflation” which is generally caused by an increase in the money supply (i.e. monetary inflation). So you would think that pumping $2 TRILLION into the economy would cause massive price inflation or even Hyperinflation.

But there are other factors involved in the creation of inflation than just the quantity of money in circulation. One of the major factors is called the Velocity of Money.

The velocity of money is the speed at which people are motivated to spend their money. During normal times people spend money when they need or want things. But during times of deflation (when prices are going down) people are motivated to hold on to their money and so the velocity of money goes down.

Conversely, during times of higher inflation (or even just the perception that inflation is coming) people are motivated to spend their money quicker before it loses some of its value. During times of hyperinflation when money loses value daily (or even hourly) such as in Weimar Germany, Zimbabwe, or Venezuela people may rush out to spend money instantly knowing that it will be worthless (or at least worth less) before long.

During the 2008-2009 market crash stocks lost over 50% of their value so people were watching their retirement plan evaporate, unemployment was skyrocketing so people were afraid of losing their jobs and/or their houses so people stopped spending money on anything that wasn’t an absolute necessity, thus the velocity of money fell drastically. This caused a waterfall effect as “luxury” businesses were forced to layoff people making the unemployment rate even worse and causing even more cuts in spending.

In addition to a decrease in the velocity of money, the market crash itself was deflationary i.e. when stock prices fall “wealth” is destroyed. In addition to ordinary individuals retirement accounts, a significant portion of the wealthy, upper-middle-class and middle-class people hold a large portion of their wealth in the stock market, so if the stock market loses a significant portion of its value these people not only feel poorer they are poorer (they can’t sell their stocks and buy as much stuff). So even though the stock market isn’t counted in most monetary calculations it is still part of the modern money supply.

So back to the question, Will the $2 Trillion COVID-19 Stimulus Cause Inflation? Or even Hyperinflation?

The answer depends on how well the deflationary forces ie. the falling stock market, decrease in spending (i.e. slower velocity of money), and the decrease in GDP due to closures are balanced against the inflationary forces of the stimulus.

The total value of the U.S. stock market was roughly $37.7 Trillion at the end of 2019. So a loss of 30% would reduce the perceived money supply by $11.3 Trillion so $2 Trillion would be only a “drop in the bucket” but if the stimulus causes the stock market to rebound to previous levels as fear of the virus abates, we then have a $2 Trillion surplus to cause inflation. But there is more to consider than just the stock market.

The GDP of the United States in 2019 was $21.4 Trillion, so if the U.S. GDP falls by 10% due to the virus, and the stock market rebounds to previous levels rather quickly, a $2 Trillion infusion would be just about right to keep inflation at current levels. Of course, if the GDP falls by 15% we could see deflation and if it only falls by 5% we could see inflation. In the deflationary scenario, the FED will probably institute more Quantitative Easing and in the inflationary scenario, the FED will institute Quantitative Tightening as conditions unfold. Quantitative easing is where the FED buys “assets” on the open market in order to pump liquidity directly into the market.

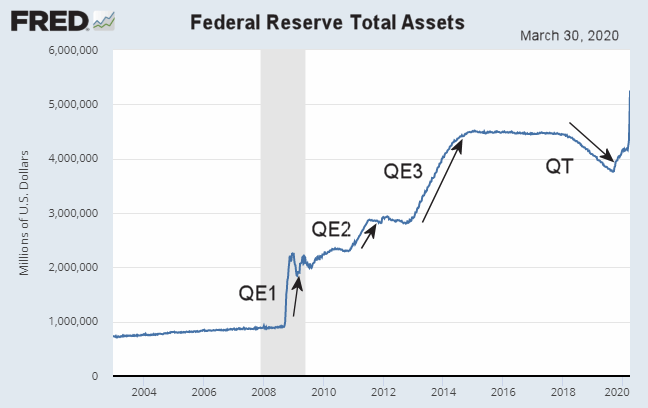

In the following chart, we can see the FED’s “Total Assets” where we can see the three previous phases of Quantitative Easing (QE) where the FED massively increased the money supply to fight the deflationary forces on the 2008-2009 crash.

Then beginning in 2018 through most of 2019 the FED began trying to unwind some of their holdings by engaging in Quantitative Tightening, which resulted in the stock market tanking and so the FED reversed course and began easing at the end of 2019. At the tail end of the chart, we can see the FED is once again instituting massive easing to combat the market crash due to the virus.

You might also like:

- How the Economy Works

- Inflation: The Hidden Tax

- 5 Reasons to Invest In Gold

- How the FED Controls the Money Supply

- Does the FED Control Mortgage Rates?

- Imports, Exports, and Exchange Rates

Hi Tim,

Thanks for the article.

However,

How can the total value of the U.S. stock market is $37.7 Trillion while the GDP of the US is $21 trillion?

Thanks

Valijon,

Excellent question! I’m assuming that you are asking why the stock market (which represents the total accumulated value of all companies over a hundred years) is only worth about 1.5 times more than the country makes in a year. I had never thought of that before so I had to think a minute. First let’s look at the formula for GDP.

GDP = private consumption + gross investment + government investment + government spending + (exports – imports). i.e. it measures total output.

So, first of all, some of the GDP is actually consumed such as the value of all the food you eat, the gas you burn, the electricity you consume, etc. Secondly, there is a lot of government consumption that produces no value, or even if it does produce value such as constructing government buildings or roads and bridges, that value isn’t counted in the value of the stock market. Currently total government spending is 37% of GDP. And that is just the federal government. You also have all the individual state governments. And then there are services both public and private such as the Post Office and FedEx once the service is performed it is just like a consumable. Over the last 30 years the U.S. has become more and more service-oriented and less product-oriented so long term it doesn’t create any tangible value to add to the stock market value. So once you subtract all of these “non-productive” factors only a very small percentage of the GDP is available to boost the stock market value.

Hope this helps!

Good and useful

The Fed had originally indicated it was going to add $700 billion to its bond portfolio — $500 billion in Treasurys and $200 billion in mortgage-backed securities. However, it switched earlier this week to an open-ended program in response to tumult in financial markets.

Wall Street now anticipates the balance sheet could hit $10 trillion this year as the Fed affirms its whatever–it-takes commitment to softening the coronavirus blow. Fed Chairman Jerome Powell told NBC’s “TODAY” show Thursday that the central bank will “aggressively and forthrightly” continue its efforts and will not “run out of ammunition.”

The impact of central bank injections will be equally enormous. For example, the US Federal Reserve may finance part of the country’s fiscal stimulus by buying Treasuries. On top of that, its balance sheet will grow from purchases of mortgage bonds and packages of private loan assets. It would not be surprising if the Fed’s balance sheet increased by $2tn-$3tn this year, up from $4.2tn at the end of 2019.