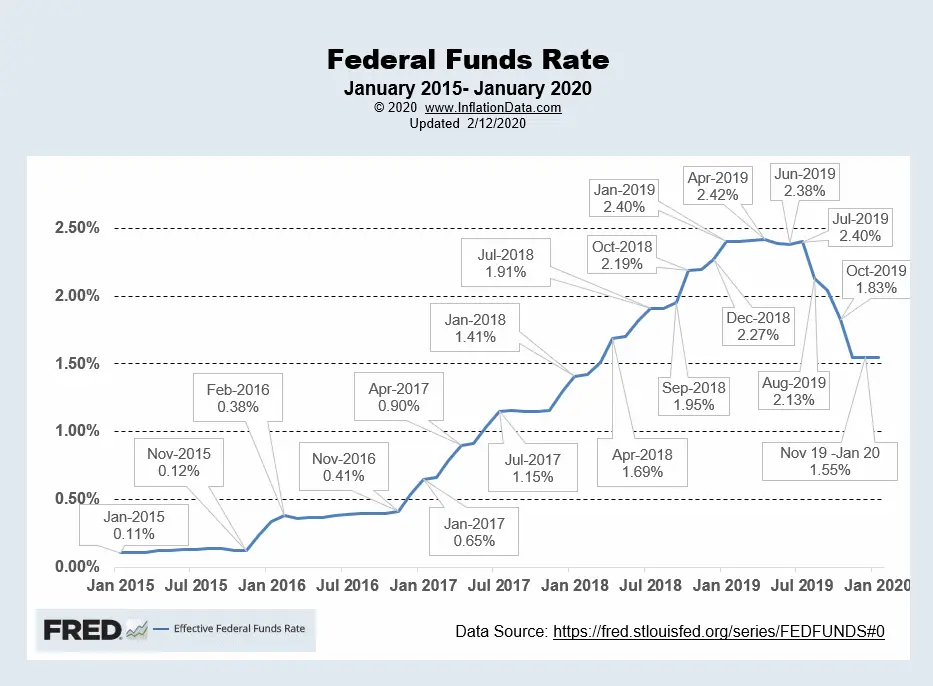

For new home buyers, anything that increases the cost of the purchase (like rising mortgage interest rates) can negatively impact your ability to be able to afford your home. That is why everyone is concerned when the Federal Reserve (i.e. the FED) raises interest rates. The following chart shows how the Fed Funds Rate has performed from January 2015 through July 2019. The FED lowered the FED Funds rate to near zero in response to the market crash in 2008-2009. It kept it there until January 2016 when it began gradually raising rates. However, at their July end meeting, they decided to lower interest rates, reducing the federal funds rate target by 25 basis points, to a range of 2% to 2.25%. This has led home buyers to hope for lower mortgage rates.

How the Federal Reserve Affects Mortgage Rates

The FED does not directly raise mortgage rates. Instead, they have a much more indirect influence on rates. The Federal Open Market Committee (FOMC) i.e. the Federal Reserve’s policymaking arm controls “federal funds rate” which is the interest rate that banks charge other banks for lending them money “overnight”. This can affect the cost of money banks pay and thus have an effect on how much they charge their customers for mortgages. If they can borrow money cheaply from other banks they will tend to lower interest rates for their mortgage customers but if they have to pay more to borrow the money they will have to charge more.

But banks typically don’t borrow money “overnight” to loan out for 20 or 30 years. That would subject them to way too much risk. Instead, most loans originate from three different Federal organizations.

- Fannie Mae (FNMA – Federal National Mortgage Association)

- Freddie Mac (FHLMC – Federal Home Loan Mortgage Corporation)

- Ginnie Mae (GNMA – Government National Mortgage Association)

Home Loan Origination

But you still work locally with banks, mortgage brokers and credit unions. They do the paperwork, run the credit check and issue the loan. They may also handle the processing of your mortgage payment or they might sell your loan to another processor.

What happens behind the scenes is that loans get “bundled” into “pools” and then sold to one of the three institutions listed above. They take the risk and the originator gets a fee for creating the loan and the servicer gets a monthly cut for handling the paperwork and collecting your money (roughly only 3/8ths of a percent) but it adds up on thousands of loans. But even Fannie, Freddie and Ginnie don’t have unlimited funds, so they end up selling the bundles to investors.

The Role of Investors

Investors are always trying to invest their money to get the best return which is some combination of risk and reward. So, they compare the rates available in the corporate bond market versus the rate available from long term Government bonds, savings deposits, and even mortgage bundles, etc. But they also consider how much risk is involved. A short-term bond has less risk than a long-term bond from the same issuer. A government bond has less risk than a corporate bond etc.

An individual mortgage has more risk than a pool of mortgages because one person may default, but it would be much less likely that the whole group would default. However, when pools the government agencies create these pools, they also group them by risk. So, there are high-risk pools of mortgages, medium risk pools, and lower risk pools. So, another factor in determining the mortgage rate is the riskiness of the pool you are put in. High-risk borrowers have to pay more for a mortgage than low-risk borrowers. But a lot of different market factors go into the process of determining mortgage rates not simply the Federal Funds Rate, including the availability of alternatives, market conditions, how much money Freddi, Fannie, and Ginnie have on hand, and even how politically motivated Congress is to promoting homeownership.

You might also like:

- How the FED Controls the Money Supply

- What Causes Unemployment?

- Marginal Utility

- What is “Leverage”?

Leave a Reply