When the government spends more money than it receives in taxes it has a “deficit” situation. In order to deal with this deficit, it engages in some fancy bookkeeping.

The government is made up of a variety of agencies, so the other agencies request money from the Treasury Department. If it doesn’t have enough money the Treasury Department issues an IOU (called a Government Bond).

The Treasury gives the Bond to the Federal Reserve (which is theoretically not part of the government). The FED writes a check to the Treasury for the bond. It then breaks up the bond into smaller bonds and sells them to individual banks.

The banks then sell them to individual investors and groups of investors (i.e. mutual funds, etc).

Another Way Money is Created

In addition to the Federal Reserve simply writing a check the commercial banking system can also create money through the “Fractional Reserve System”. Whenever people borrow money, banks are actually creating money out of nowhere. Although banks are required to maintain a small fraction of their assets with the Federal Reserve (i.e. reserve requirements).

Banks with less than $15.2 million in assets are not required to hold reserves. Banks with assets of less than $110.2 million but more than $15.2 million have a 3% reserve requirement, and those banks with over $110.2 million in assets have a 10% reserve requirement.

The idea is that not everyone is going to run to the bank and want to get all their money out all at once so, (unless there is a panic) so banks only need to keep a fraction on hand to cover those requests. The rest of the money can be loaned out to earn a profit. At first glance, you might wonder how this is creating money.

How Fractional Reserve Creates Money

When you deposit $10,000 in a big bank they can loan out 90% of it, so they turn around and loan out $9,000. So you might think that your money just went to the borrower just as if you had bought something from them.

But that is not the case. If you had bought something you would have a thing and no money but in this case, you still have your money (as an IOU from the bank) and the borrower also has the money as a loan from the bank.

But it doesn’t end there. The borrower then takes the $9,000 to a neighbor and buys a used car. The neighbor takes that money and puts it in the bank. The bank then loans out 90% of $9,000 or $8,100. And the cycle continues creating $7,290 and $6,561 and $5,904.90 and on and on.

There is actually a formula for calculating how much money will ultimately be created through a fractional reserve system, it is:

Initial Deposit x (1 / Reserve Requirement) = Total Money Created

So, for a 10% reserve requirement (0.10) the formula would look like this:

$10,000 x (1/0.10) = $100,000.00

So, each $10,000 can actually become, $100,000.

But what about the smaller banks with a 3% reserve requirement?

In that case the formula would be $10,000 x (1/0.03) = $333,333.33

If everyone deposited their money into smaller banks the initial $10,000 would actually become over $300 Thousand dollars.

How the FED Controls the Money Supply

As we saw, the FED can either print money by simply writing a check or it can adjust the Fractional Reserve Requirement. If they lower the requirement from 10% to 3%, they would effectively triple the multiplication factor. But they would also make the whole economy more likely to fail as more risky investments would be made.

Another problem is that the multiplication might not happen at all… due to risk aversion. After the crash of 2008 banks were reluctant to loan money and borrowers were reluctant to borrow, so no borrowing means no fractional reserve multiplication. Economists call this “Pushing on a String” it just doesn’t work.

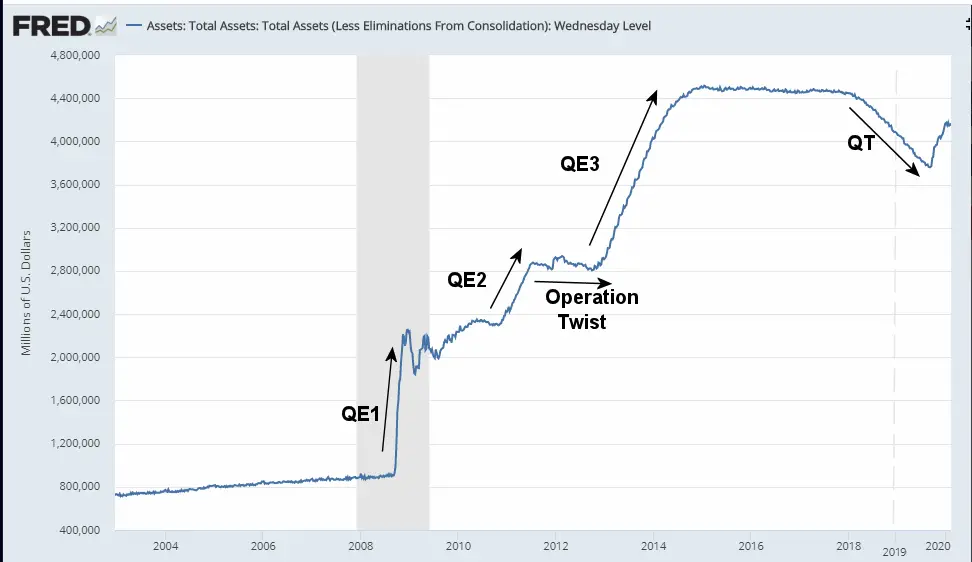

So, the FED had to come up with another way to inject money into the economy. And so, they invented “Quantitative Easing”. In quantitative easing the FED bought up junk bonds and a variety of other debt instruments that the market was reluctant to accept and instead wrote a check for them. So, they converted illiquid bonds into ready cash. In the table below we can see how QE1, QE2 and QE3 affected the assets held by the FED.

In the chart above, we can also see the FEDs attempts to reduce their holdings by allowing expiring assets to not be replaced in a move called Quantitative Tightening (QT).

You might also like:

- What is the Real Definition of Inflation?

- What is Core Inflation?

- What is Hyperinflation?

- What is “Leverage”?

- What is the Difference Between Micro and Macro Economics?

Leave a Reply