With inflation reaching heights not seen in many years, people are wondering… How to prepare for inflation? And What effects will inflation have on our investments? Between 2020 and 2021, inflation steadily increased from a minuscule 0.12% in May of 2020 to just under 5.4% in June and July of 2021. Although 5+% may not seem like much, it means that prices are 5% higher than they were a year ago. If inflation stays at 5%, you might think it has stabilized, but unfortunately, inflation compounds. So if the inflation rate is still at 5%, next year’s prices are now more than 10% higher than last year. So, for instance, after 1 year at 5% inflation, a $100 item now costs $105, but after another year, it costs $110.25… at that rate, prices will DOUBLE in a little over 14 years.

Purchasing Power- Preparing for Inflation

The flip side of inflation is purchasing power. At 5% inflation, every year, your money buys 5% less. This is especially troubling for retired people living on “fixed incomes” or living off of savings. According to the Motley Fool, the average retirement lasts 18 years, so if 14 of those years have 5% or more inflation, annual expenses for the average retiree will more than double during their retirement years.

Social Security- COLA

Social Security is supposed to have a COLA, aka. “Cost of Living Adjustment” but the COLA is based on the CPI-W (CPI For Urban Wage Earners And Clerical Workers) rather than the more typical CPI-U (Consumer Price Index for all Urban Consumers) or the CPI-e (Consumer Price Index for Elderly), which more closely tracks medical expenses and other typical expenses of the elderly. The CPI-W is the older index, and the Bureau of Labor Statistics added the CPI-U in 1978 to cover a larger segment of the population. The CPI-e covers a smaller segment of the population and is still considered “experimental”. It is estimated that using the CPI-E as the COLA adjustor instead of the CPI-W would increase payouts by more than 4% over a 30-year period.

| YEAR | COLA |

| 1995 | 2.6 |

| 1996 | 2.9 |

| 1997 | 2.1 |

| 1998 | 1.3 |

| 1999 a | 2.5 |

| 2000 | 3.5 |

| 2001 | 2.6 |

| 2002 | 1.4 |

| 2003 | 2.1 |

| 2004 | 2.7 |

| 2005 | 4.1 |

| 2006 | 3.3 |

| 2007 | 2.3 |

| 2008 | 5.8 |

| 2009 | 0.0 |

| 2010 | 0.0 |

| 2011 | 3.6 |

| 2012 | 1.7 |

| 2013 | 1.5 |

| 2014 | 1.7 |

| 2015 | 0.0 |

| 2016 | 0.3 |

| 2017 | 2.0 |

| 2018 | 2.8 |

| 2019 | 1.6 |

| 2020 | 1.3 |

a The COLA for December 1999 was originally determined as 2.4 percent based on CPIs published by the Bureau of Labor Statistics. Pursuant to Public Law 106-554, however, this COLA is effectively now 2.5 percent.

The first COLA, for June 1975, was based on the increase in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) from the second quarter of 1974 to the first quarter of 1975. The 1976-83 COLAs were based on increases in the CPI-W from the first quarter of the prior year to the corresponding quarter of the current year in which the COLA became effective. After 1983, COLAs have been based on increases in the CPI-W from the third quarter of the prior year to the corresponding quarter of the current year in which the COLA became effective.

Inflation Hedging Strategy

When people think about hedging against inflation, they tend to think of buying gold or silver, but what if your funds are limited and you can barely afford daily expenses?

One of the best personal finance inflation protection strategies is also a good strategy for protecting against all sorts of other emergencies. And that is simply to stockpile non-perishable items. As I said in my recent Article Be Prepared or Else, stockpiling things when they are cheap and readily available can be a good strategy. And if you know they will be 5% more expensive next year, it is like getting a guaranteed 5% return on your investment.

If you have the storage space, buying things that you are sure you will need next year can save you a bundle of money. These days with warehouse stores like Price Club, Sam’s, and BJ’s, it is easy to buy in bulk. So you could buy extra detergent, coffee, peanut butter, or whatever you typically use, and a year from now, you will be happy that you got to buy it at a much lower price.

Back in 1981, John Pugsley wrote a book entitled “The Alpha Strategy: The Ultimate Plan of Financial Self-Defense,” which promoted the idea that the best defense against rampant inflation was commodities. He said, “Instead of converting labor into money, money into investments, investments back into money and money into real goods once again, convert your surplus earnings directly into real goods.”

Pugsley was not a survivalist “prepper” like Howard Ruff of the same era. Pugsley simply believed that buying stuff before you need it was a good use of your money. He also favored investing first in your education, skills, and tools. Second in non-perishable consumables. And finally, if you have any money left, invest in hard assets. Pugsley recommended food that you would eat over the next year, like canned goods with at least an 18-month shelf-life. Sugar which will keep almost indefinitely, tea, dried beans, and pasta. One of Pugsley’s ideas was to store things that had the highest value per cubic foot. So since toilet paper is rather voluminous, it would be low on his list. However, considering recent experience, it might be worth stockpiling some… just in case.

High Inflation Investing Strategy

The best investments for inflation have always been considered precious metals because they are NOT paper assets, i.e., they are physical and not simultaneously someone else’s liability. However, as we showed in Gold and Inflation, Gold is more of a crisis hedge than an inflation hedge. “In times of uncertainty, investors turn to Gold as a hedge against unforeseen disasters” of course, inflation causes some uncertainty, i.e., how much will my money depreciate over the next 1, 5, or 10 years? But wars, political unrest, riots, market crashes are all forms of uncertainty that tend to drive prices of gold up as well. Interestingly, long steady (but relatively high) inflation did not affect gold as rapidly changing inflation levels. But being a commodity, gold tends to maintain its purchasing power better than paper assets.

Other inflation protection strategies include buying oil, certain stocks of companies that do better in an inflationary environment, and Treasury Inflation-Protected Securities (TIPS). You can either buy these directly from the government or buy something like Fidelity inflation-protected bond index fund (FIPDX). “An inflation-indexed bond adjusts the underlying principal balance based on an inflation index like the CPI-U.” So, during high inflation years, your principal would be increased to offset the loss of value due to inflation. Although it doesn’t pay as much interest to start in practice, the benefit is not as great as you might think it would be.

Inflation Strategy Funds

Some industries like airlines do not do well during periods of high inflation because the high cost of fuel makes operations unprofitable. But mining and oil companies tend to do well. So following a strategy that invests in a fund specializing in these industries can be a profitable inflation portfolio strategy. Other investment strategies for high inflation include Real Estate, either directly or through Real Estate funds, REITs, or companies that hold large quantities of real estate, such as timber companies.

Another inflation protection strategy is to convert some of your savings to another less inflationary currency. For instance, when Argentina, Brazil, or Zimbabwe suffered from hyperinflation, those with liquid assets would invest in U.S. Dollar-denominated assets; even just a savings account that paid low interest was better than keeping your money in a rapidly depreciating currency. During the 1980s, when the U.S. Dollar was undergoing high inflation, Americans followed the inflation management strategy of putting their money in Swiss francs to help it retain its value.

Best Investments to Prepare for Inflation

- Hard assets – like gold, silver, platinum, and other metals including Lithium

- Strategic Metals– like Galium, Indium, Germanium, Hafnium.

- Commodities – either physically or in a Commodity Fund

- Materials Companies – Including chemicals, steel, lumber, paper, mining, etc.

Worst Investments for Inflation

- Transportation- Airlines, Trucking, high fuel costs might cut into profits.

- Rent Controlled Apartments- Expenses go up, but income stays the same.

- Regulated Industries

- Industries with high feedstock costs, i.e., that use a lot of steel, lumber, etc.

Inflation Finance

One of the interesting things about “inflation finance” is that it tends to turn everything upside down. In a normal environment, debt is bad, and being debt-free is good. But in a highly inflationary environment, being in debt can actually be an advantage. This is because if your interest rate is fixed, you get to pay your debt back with cheaper dollars. So if you buy a house and you have a 30 year fixed mortgage at 4%. So if inflation is 5%, you are actually coming out 1% ahead just compared to the interest (if your salary keeps up with inflation). But as we said earlier, after 14 years, you will be paying back the principal with dollars that are only worth half of what they were when you bought the house. And after another 14 years, your final payments will be practically nothing compared to the value of the dollars you originally borrowed.

To take advantage of this strategy, you might want to buy rather than rent or even refinance your home mortgage if you already own a home.

FED Inflation

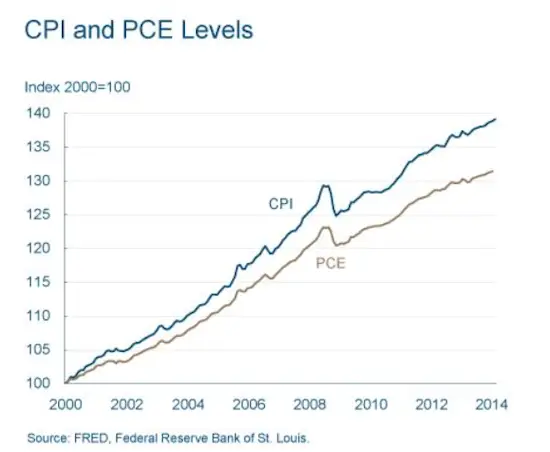

The Federal Reserve inflation indicator is the “PCE” rather than the Bureau of Labor Statistics CPI. The Personal Consumption Expenditures price index (PCE) is issued by the Bureau of Economic Analysis and used more by the FED. The PCE has been consistently lower than the CPI, as we can see from the chart below.

Some of the difference between the two indices is attributed to the weighting given to the individual components. As we mentioned earlier, the CPI-e for the elderly gives more weight to things the elderly have to pay for, such as health care, while the CPI-U gives more weight to things that impact Urban Consumers, such as rent and transportation. The CPI-U is based on a survey of what households are buying; the PCE is based on surveys of what businesses are selling. The PCE gives more weight to things that Consumers don’t pay for directly, such as paid medical care by employer-provided insurance.

Some of the difference between the two indices is attributed to the weighting given to the individual components. As we mentioned earlier, the CPI-e for the elderly gives more weight to things the elderly have to pay for, such as health care, while the CPI-U gives more weight to things that impact Urban Consumers, such as rent and transportation. The CPI-U is based on a survey of what households are buying; the PCE is based on surveys of what businesses are selling. The PCE gives more weight to things that Consumers don’t pay for directly, such as paid medical care by employer-provided insurance.

Both the CPI and the PCE can be sliced and diced in various ways. By stripping out food and energy, you get the “CORE” CPI and “CORE” PCE. Eliminating these volatile elements can make it easier to see the underlying trend.

Therefore, the FED gives more attention to the stripped-down “core” PCE that doesn’t include Food and Energy because that will indicate how their monetary policies affect prices. See: What is Core Inflation and Why Doesn’t It Include Food and Energy? for more information.

You might also like:

- Safe-Haven Investments that Protect Your Capital From Rising Inflation

- 9 Inflation Books You Must Read

- Hyperinflation Strikes Lebanon… Again

- BLS says July Inflation Holds Steady at 5.4%

- The Relationship Between Inflation and Interest Rates: Explained

- How Can Inflation Affect Businesses?

- Inflation and Bonds

Do you do your own financial planning for retirement? If so, what inflation rate do you use for your annual budgeted living expenses ?

Paul,

That is an excellent question! Up until recently, I used 3 – 3.5% since that is the long-term range. But if we are entering a period of higher inflation I may need to adjust that upward. A lot depends on your timeframe. If retirement is in the next 10 years you might want a higher level if it is 30 years you might want to stick with the long-term average. Hope this helps.

i,m very thankful for your articles.

You present a well balanced article which I found logical and answer’s many of my queries.