History of Central Banking

History of Central Banking

Like everyone, kings like to spend money, whether it is to wage war or to build palaces, but they often didn’t have all the money they “needed”, so they had to borrow it. To facilitate this large scale borrowing, they created a Central Bank to handle that function. In 1790, “Federalist” Alexander Hamilton advocated for a Central Bank in the United States.

Democratic-Republicans, Thomas Jefferson and James Madison believed that the Constitution did not grant the Federal government the authority to create a bank, based on the 10th amendment i.e. that all powers not endowed to Congress are retained by the States (or the people). But Hamilton argued that although not specifically mentioned, the Constitution’s “necessary and proper” clause implied that such a bank could exist. Jefferson rejected the idea that the Bank was truly necessary or even desirable. Both he and Madison also feared that the Bank would be a tool that urban Northern interests could use to dominate the agrarian South. Jefferson’s tour as ambassador in France in the 1780s, during the waning years of the Bourbon monarchy, helped to form his conviction that powerful, centralized governments are prone to corruption, debt, and ultimately tyranny. And Centralized banks were a key component of that tyranny. Jefferson advocated for decentralized banking under the control of the individual states.

Despite Southern objections, Congress passed the bill granting a 20 year charter to the “First Bank of the United States” which was modeled after the Bank of England and given the monopoly privilege of its notes being the only acceptable form of payment for tax payments to state and federal government, and no other banks were permitted to operate in the country.

According to Murray Rothbard History of Money and Banking in the United States The First Bank “pyramiding on top of $2 million in specie” issued millions of dollars in paper money and demand deposits and “promptly fulfilled its inflationary potential.” It invested heavily in the US government, and “The result of the outpouring of credit and paper money by the new Bank of the United States was … an increase [in prices] of 72 percent” from 1791–1796. So, when the bank’s 20-year charter expired in 1811, Congress refused to renew it by one vote.

The Second National Bank

Five years later, in 1816, Congress tried again. The charter for the Second Bank of the United States was passed by a narrow margin. But by the time Andrew Jackson was elected President in 1828 popular opinion was once again turning against a central bank. So Jackson pursued a policy to end the bank. In 1832, he vetoed a bill calling for the early renewal of the Bank’s charter. And he instituted a policy whereby effective October 1, 1833, federal funds would no longer be deposited in the Second National Bank but instead would be deposited in various State banks.

In an effort to fight back, the President of the Second Bank, Nicholas Biddle, started presenting state banknotes for redemption, calling in loans, and generally contracting credit. He hoped that a financial crisis would demonstrate the need for a national bank. This battle between Jackson and Biddle became known as the Bank War, and became the hot topic among Congress, the Press and the public. In the end, Biddle’s ability to disrupt the economy worked against the central bank in the mind of the public and the Second Bank’s charter expired in 1836.

Free Banking

From 1836 through 1865, banking was handled through State-chartered banks and unchartered “free banks”. During this period banks issued their own notes redeemable in gold or specie. Toward the end of this period the Civil War resulted in massive inflation primarily in the South. Confederate Inflation Rates (1861 – 1865).

During the Civil War, the National Banking Act of 1863 was passed, providing for nationally chartered banks, whose circulating notes had to be backed by U.S. government securities. An amendment to the act required taxation on state bank notes but not national bank notes, effectively creating a uniform currency for the nation. Despite taxation on their notes, state banks continued to flourish due to the growing popularity of demand deposits, which had taken hold during the Free Banking Era.

Stress from the Civil war and uncontrolled fractional banking resulted in a banking panic in 1893. Another round of speculation on Wall Street in 1907 set the stage for “banking reform”. The Aldrich-Vreeland Act of 1908, provided for the emergency issue of currency during a crisis. In late 1910, a group of bankers held a clandestine meeting to plan a bill for the formation of the Federal Reserve at a “Duck Hunting Reserve” on Jekyll Island, GA. Although they were planning a “Central Bank” for political reasons they presented it as “decentralized”. Eventually, this plan became the Federal Reserve Act passed in December 1913. Not so coincidentally the Federal Income Tax was instituted earlier that same year.

The Federal Reserve

In the United States, the Central Bank is called the Federal Reserve or FED. In the U.K. it is the Bank of England (BoE) and in Japan, it is called the Bank of Japan (BoJ).

In the United States, the Central Bank is called the Federal Reserve or FED. In the U.K. it is the Bank of England (BoE) and in Japan, it is called the Bank of Japan (BoJ).

A central bank, also known as a reserve bank, is an institution designed to serve several various and often conflicting functions. The primary reason that central banks were originally created was to be the bank for the government.

However, over the years other functions have been added to the basic “banker to the government” role. Beginning in 1977 Congress imposed a “Dual Mandate” on the Fed requiring both price stability and full employment. These two mandates are polar opposites however, so the FED has a bit of a balancing act to maintain the best balance possible.

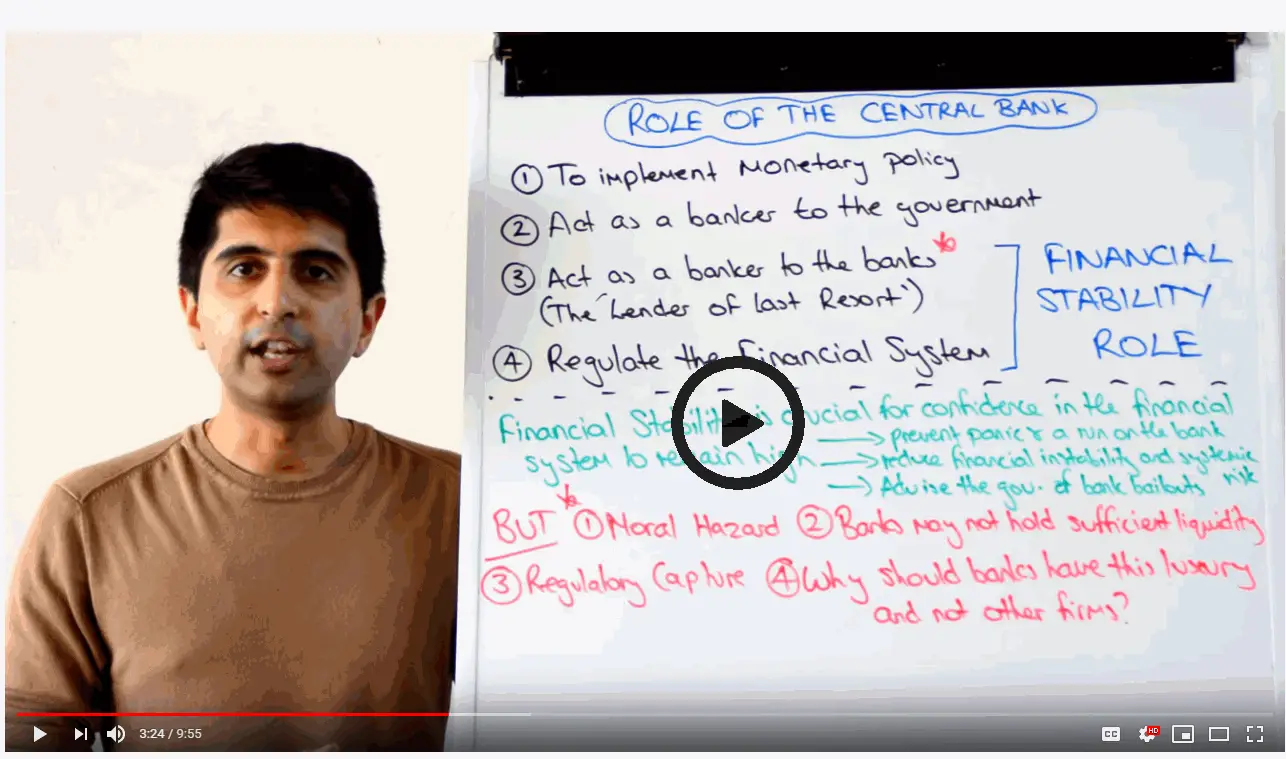

Other functions of the Central Bank include:

- Implement Monetary Policy

- Act as a banker to Banks

- Regulate the Financial System

Act as a Banker to the Government

The FED and other Central Banks still act as the Banker for the Government lending it money to wage wars or create social welfare programs. When the government runs a deficit, it has to get the money somewhere and this is achieved through a complex money shuffle done by the Federal Reserve.

Implement Monetary Policy

“Monetary policy” is the methods in which the Central Bank controls inflation, money supply, economic growth, price stability, and liquidity.

Central banks use a variety of different methods to achieve these goals. Things, like modifying interest rates, regulating foreign exchange rates, and changing the amount of money banks, are required to maintain as reserves. They can also increase or decrease the supply of government bonds by either being a net buyer or seller of the bonds. This can increase or decrease the amount of money in the banking system.

In “Operation Twist” the U.S. FED was neither increasing or decreasing the money supply. Instead they wanted to fight an inverted yield curve. They did this by buying long-term bonds and selling short-term bonds. In an effort to decrease short-term interest rates and increase long-term rates.

Foreign Exchange Rates

Up until 1992, most Central Banks fixed their exchange rate against foreign currencies by law but beginning in 1992 Central Banks abandoned that practice in favor of allowing the rate to be determined by the free market on FOREX exchanges. Some Central Banks like the Central Bank of China, however, still set their Exchange rate by fiat. This “arbitrary” setting can cause adverse forces in the economy.

Act as a Banker to Banks

As the banker to banks, the FED has a variety of functions. It sets interest rates through its FED Funds rate which is the rate that banks can borrow each other’s “excess reserves” that are actually held by the FED itself.

The FED is also the “Lender of Last Resort” which means that if a bank can’t borrow from other banks it can always borrow directly from the FED itself. This borrowing is done at the “discount Rate” which is also set by the FED but is higher than the FED Funds Rate.

Some Central Banks also provide deposit insurance to help maintain confidence in the banking system and prevent “runs” on the banks. Although the U.S. FED doesn’t provide this type of insurance to the U.S. banking system there is another independent federal agency insuring deposits in U.S. banks called the Federal Deposit Insurance Corporation (FDIC).

One disadvantage of policies like Lender of Last Resort and Federal Deposit Insurance is that banks can see this as a license to take more risk and thus create instability in the entire banking system as we saw in 2008. For this reason, the FED also has a regulatory role.

Regulate the Financial System

The FED requires its banks to maintain a certain percentage of their funds in reserve. In other words it must not lend out 100% of its money. And the FED doesn’t just take a bank’s word that they have these reserves. Instead, the banks must keep their required reserves in the FED’s bank. The bank gets no interest on these reserves, so if it has any excess over the required minimum it will loan that to another bank with a shortfall. This lending is done at a rate very close to the FED’s recommended “FED Funds Rate”.

Different countries use different methods to monitor and control their banking sector. The U.S. uses several different agencies. The three main 3 federal agencies are, the Federal Deposit Insurance Corporation, the Federal Reserve Board, and the Office of the Comptroller of the Currency plus others on the state and the private level.

For more information:

- Wikipedia: The First Bank of the United States

- Misses.Org: The Corrupt Origins of Central Banking

- Federal Reserve: History

You might also like:

- Inflation: The Hidden Tax

- How the Economy Works

- Does the FED Control Mortgage Rates?

- Imports, Exports, and Exchange Rates

- Will the $2 Trillion Covid-19 Stimulus Cause Inflation?

- What Impact Does Interest Rates and Inflation Targets Have on Stocks?

Leave a Reply