At its June 15th meeting, the FED announced that it will be raising rates by ¾%. Up until last week, this would have been a big shock to the market. But despite the imposed FED silent period leading up to their Wednesday meeting “somehow” journalists from all the major financial publications published remarkably similar articles predicting a 0.75% increase in the FED funds rate. Prior to this leaked guidance, the consensus was that the FED would increase rates by ½% but last week’s higher-than-expected inflation report threw a wrench into the works.

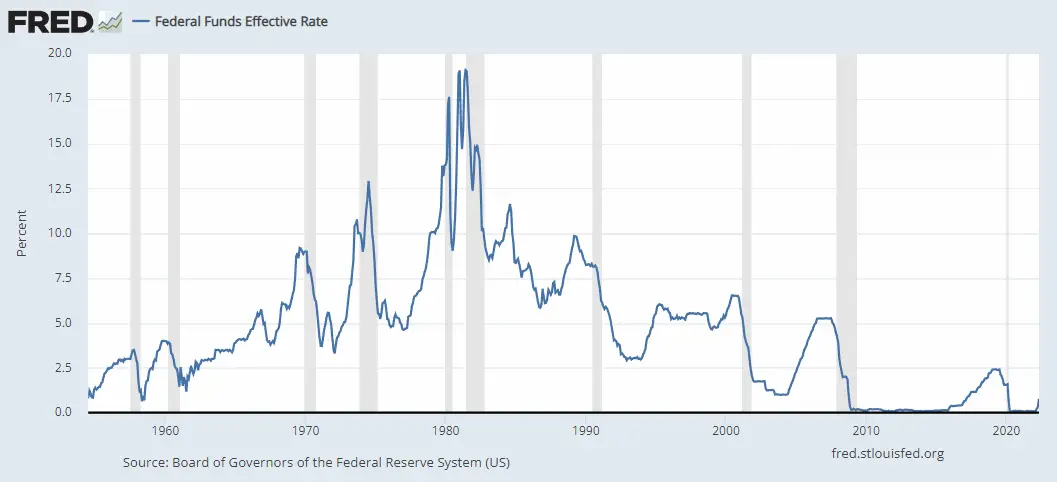

Everyone is making a big deal out of the fact that this is the first raise of that magnitude since 1994. And that it will double the FED funds rate. Liz Ann Saunders of Schwab wrote an article entitled “The FED Goes for Inflation’s Jugular with 0.75% rate hike” like that was some major feat. What they aren’t saying is that the FED funds rate is still ridiculously low on a historical basis. And if the FED had started acting a year ago as they should have, they could have increased it at a more gradual pace. Looking at the chart below we can see that even if the FED follows through and the rate doubles from 0.75% to 1.5% it would still be only a little over half of the 2.5% of 2019.

Even 2.5% wouldn’t do much to curb the current inflation. Maybe if rates get up to 5% like they were in 2007 they would have some effect but as Jeffrey Tucker says, “the Fed has a very very long way to go before it can demonstrate that it is serious about restraining inflation”… it is like the FED is trying to put out a house fire by squirting a little water here and there.

Even 2.5% wouldn’t do much to curb the current inflation. Maybe if rates get up to 5% like they were in 2007 they would have some effect but as Jeffrey Tucker says, “the Fed has a very very long way to go before it can demonstrate that it is serious about restraining inflation”… it is like the FED is trying to put out a house fire by squirting a little water here and there.

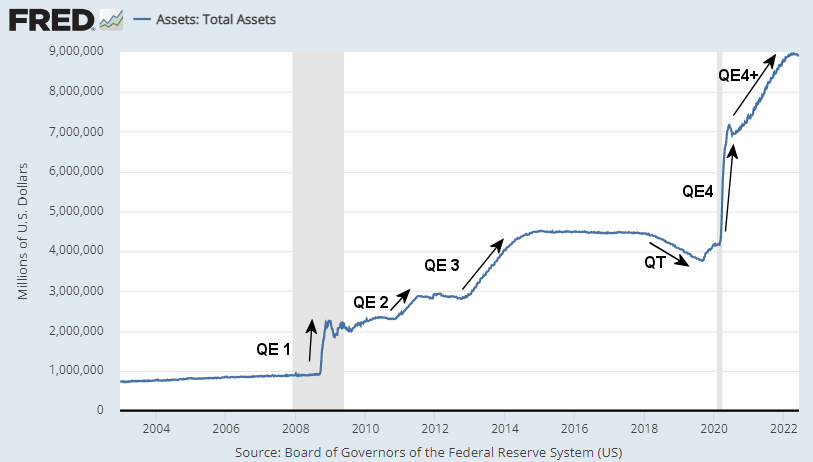

What might indicate that the FED is a bit more serious than their rate increases is their balance sheet reductions. Once again according to Liz Ann Saunders, “The FOMC confirmed its previously laid-out plan on balance sheet reduction, which just began at the beginning of June—shrinking its holdings of Treasury and mortgage-backed securities by $47.5 billion per month until September, and then upping that to $95 billion per month thereafter.”

One point where I agree with Liz Ann is her statement, “The Fed’s projections still suggest a soft landing, but a much bumpier one. We continue to believe a recession is more likely than a soft landing… The tightening in financial conditions continues to point to a meaningful economic slowdown; first-quarter real GDP growth was already negative, and now expectations for second-quarter growth are at the zero line. Powell reinforced that the Fed is “not trying to induce a recession,” but it may be a necessary ingredient in the lower inflation recipe.”

If the FED follows through we should be in a full-blown recession just in time for the mid-term elections. Currently, the only bragging point the current administration has is that unemployment is near historic lows. But as former Treasury Secretary Larry Sommers said, “We have a massive, overheated labor market… We have the highest ratio of vacancies to unemployment in the country’s history, by a large margin. We have shortages of labor, in everything from psychotherapy, to McDonald’s, in everything from investment analysts to gardeners, that suggests a surfeit of purchasing power and demand relative to the capacity of the economy to produce, and unless we bring those things into balance, we’re going to have not just higher inflation, but possibly even accelerating inflation. And we need to recognize that we have an overheated economy that we are going to need to cool off.”

In other words, the low unemployment rate is a symptom of the overheated economy, not something to be proud of.

You might also like:

- Inflation Takes a Bite Out of Your Food Budget

- Inflation Adjusted Gasoline Hits New High

- Worldwide Inflation by Country 2022

- Analyzing 5 Ways You Can Hedge Against Surging Inflation

- Roots of Our Current Inflation

Thanks. Good article.