In the last few years, housing prices have skyrocketed, and investors are once again jumping on the housing bandwagon as an excellent way to make money. The same sentiment existed in the early 2000s as housing prices were rising rapidly then as well. These periods both created the impression that “housing prices always go up”. But is that actually true?

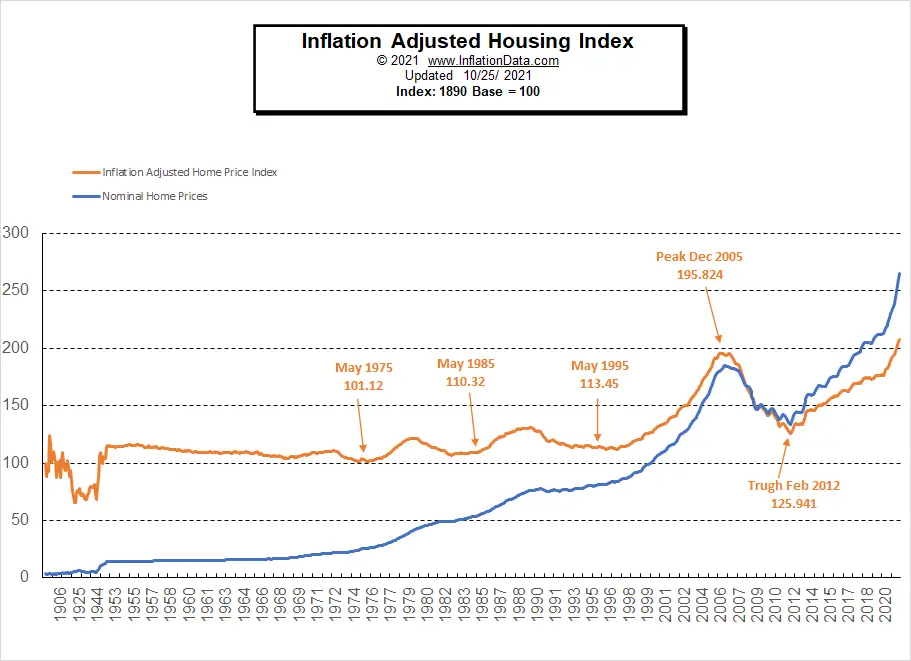

If we look at the “nominal” prices of houses, i.e., the cost in dollars BEFORE adjusting for inflation, it does appear that housing prices go up fairly consistently. In the following chart, we see housing prices since 1890. The blue line is the nominal housing price, and we can see a very gradual increase up through the early 1970s. Prices increased faster in the 1980s then leveled off during the 1990s before shooting up very drastically during the early 2000s. But then along came the crash and “the great recession,” and housing prices fell drastically.

Inflation-Adjusted Housing Prices

Inflation-Adjusted Housing Prices

However, if we look at the inflation-adjusted prices, we get a different picture. This chart adjusts housing prices by setting the 1890 housing price to 100 and compares all other prices to that base. Looking at the orange line on the above chart, we can see that from 1890 through 1975, housing prices were virtually flat except during the Depression Era. For much of that period, inflation-adjusted housing prices actually trended down slightly.

However, shortly after the U.S. closed the gold window in 1971, housing prices began increasing. Over the next 20 years, inflation-adjusted prices rode an ever higher roller-coaster. But then, even inflation couldn’t keep up with housing prices. So, although housing through much of the 20th century wasn’t a great way to make money, it was an excellent inflation hedge and, for many Americans, one of the few savings programs they had.

The Rise of McMansions

With the increase of two-income households, families could afford larger houses and McMansions became popular. This resulted in an increase in the average home size which accounts for much of the increase in house prices. So, although the cost per square foot may have only increased slightly, the average house price increased because the average house got larger. But there were also economic incentives created by the government that put in place the conditions that created the housing bubble and the subsequent crash. These included loose lending practices, government subsidies, and an aftermarket for mortgages that allowed lenders to collect fees for writing mortgages, but then offload the risk of those mortgages to others.

From the peak to the trough in 2012, builders were building very few new houses. So, the excess supply dried up, foreclosed houses were repaired, and people began buying homes again. And adjusted prices started rising rapidly on a sea of government-printed money.

For a more in-depth look at these factors, see our updated article: Inflation-Adjusted Housing prices

For a more in-depth look at these factors, see our updated article: Inflation-Adjusted Housing prices

See Also:

- How Does Inflation Affect the Price of Gold?

- Is Gold an Inflation Hedge?

- Which is Over Priced? Oil or Gold?

- The Making of the Next Housing Crisis

- Who Killed the 2007 Housing Market?

- Cost-Effective Options for Small Family Housing

- How to Combat Rising Housing Costs as a Prospective Homeowner

- Housing Trends 2012- Where are the Home Buyers?

- Ways Inflation Affects the Real Estate Market Pt1, Pt. 2

- Monetary Inflation vs. Price Inflation

- How Much Has Inflation Affected Mortgage Rates in the Last 5 Years?

- The Quantity Theory of Money

- How “Excess Reserves” and the Money Multiplier Could Trigger Inflation

Leave a Reply