The FED Giveth and the FED Taketh Away

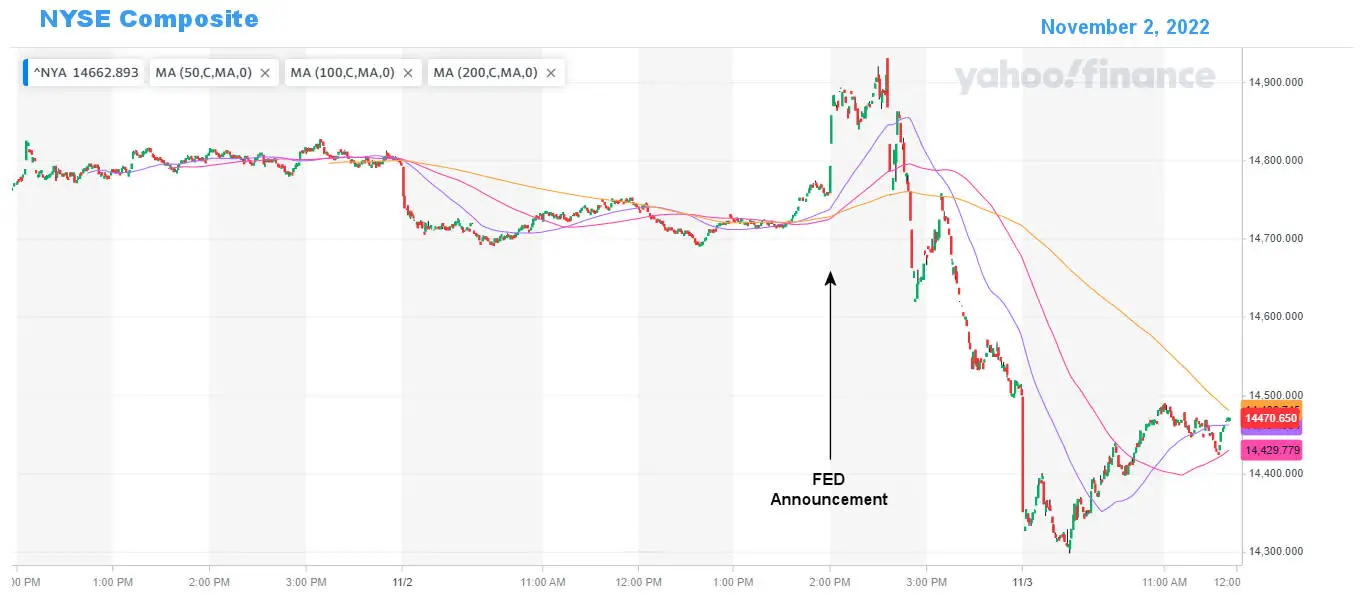

On Wednesday, November 2nd, the FED held its “Federal Open Market Committee meeting” and made the announcement the market has been breathlessly awaiting. As expected, Chairman Jerome Powell announced a hike of 75 basis points in the fed funds rate. Along with the announcement, the market was hoping for some indication of a “pivot”, i.e., that the FED would give some indication that it was going to be slackening off on its rapid rate increases.

And in this respect, the November FED Announcement did throw the market a bone. It added the new phrase “Cumulative Tightening” to the standard announcement. So, going forward, the FED will take the fact that it has already raised quite a bit into its calculations. In addition, the FED emphasized that it was still focused on being “sufficiently restrictive to return inflation to 2 percent over time”. Apparently, the phrase that the market latched onto was “Cumulative Tightening,” and it took this as a signal that the FED might, possibly, not raise so aggressively in the future.

So, the market started by rallying by 1% over the next 30 minutes.

Click for a Larger Image

But then reality and the rest of the FEDs announcement began to sink in. Powell also said, “We still have some ways to go. And incoming data since our last meeting suggests that the ultimate level of interest rates will be higher than previously expected.” Oops, so this isn’t a “pivot” or even a precursor to a pivot, but actually, it is a signal that rates may have to go higher (not lower as the market hoped) than expected.

Powell said inflation fighting via raising interest rates involves three stages:

- How fast to raise them

- How high to lift them

- How long to keep them there

Powell implied that after the fourth straight 3/4% rate increase, we’re now in Phase II. So the market is hoping that means there will “only” be a 1/2% raise next time. But Powell left the “how high” and “how long” questions to be determined at a later date. Which is the real kicker.

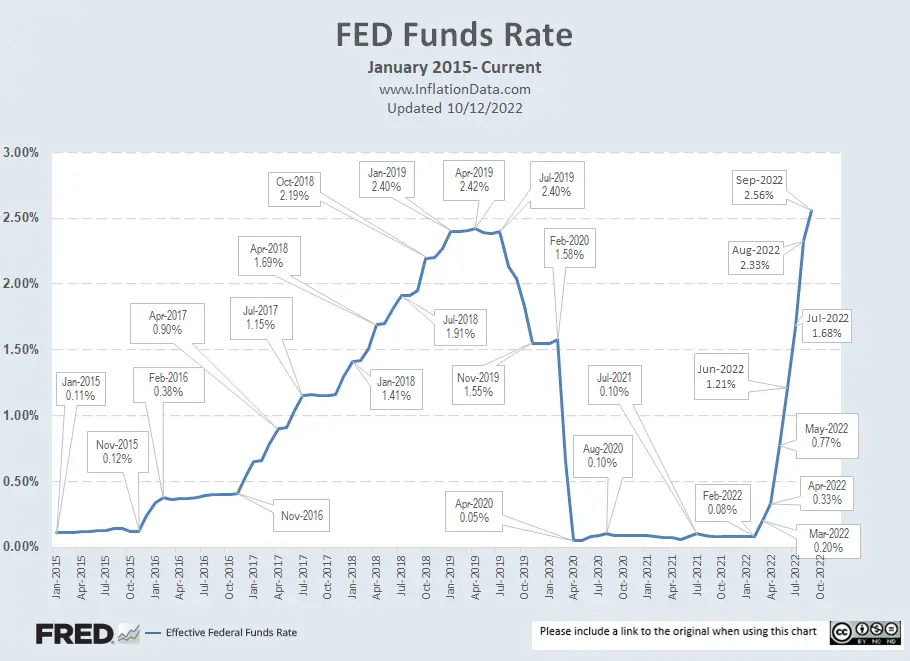

Rates Must Go Higher

Incidentally, we have been saying for quite a while now that rates were going to have to go higher than the FED has been saying, (or the market predicting), in order to get inflation under control. Typically, rates need to be higher than the inflation rate. With inflation hovering around 8% and the FED Funds rate under 3%, there is still a big gap to fill. Even if inflation comes down to 6%, the FED Funds rate would have to more than double from here.

Powell went on to say that the question of when they start slowing the pace of increases was “much less important” than how high they need to be at the finish. So, yes, it’s possible the Fed would slow down, but the key factor was the peak rate, and Powell was indicating that there was probably a long way to go.

This sparked the market to raise their estimates of future fed funds rates. Their expectation of the peak, probably reached by May of next year, is for the first time above 5% (which is still below our estimates of the FED funds rate peak).

Powell continued with the bad news by including, that so far, they hadn’t tightened too fast, they aren’t “too tight”, and, “It’s very premature to think about or talk about pausing our rate hikes.”

The only bright spot in the announcement for me was that Powell seemed to hint that central bankers understand that there is a significant lag between raising rates and the effects of those raises, and that they need to check what effect their moves are already having before hiking further. So they may be cautious about overreacting and raising too quickly.

So the FED first gave the market hope, and then rather quickly dashed those hopes, as the reality of the entire statement sunk in.

You might also like:

- Jerome Powell “Channels” His Inner Paul Volcker

- September 2022 Inflation Virtually Unchanged

- September Unemployment Falls… Dragging Market Down

- Latest Recession Alarm

Leave a Reply