We’ve been a bit spoiled over the last couple of decades because inflation has been relatively tame. The first thing to remember about inflation is that it is primarily a loss of purchasing power. That means that to keep up with inflation, you need to have “more money” in other words, with 7.5% inflation, you have to have $107.50 next year to be able to buy the same thing you could buy for $100 this year. So the first rule of inflation is “don’t lose purchasing power”.

But unless you can earn at least 10% on your money, you are probably losing ground. Why 10%? Because you still have to pay taxes on your gain. If you invest $100 and make 8% i.e. $8 and then have to pay the government 20% of your gain in taxes $8 x .2 = $1.60 so your $100 “grew” to $100 + $8 – $1.6 = $106.4 which actually buys less than your $100 bought the year before. So you ended up paying taxes on a “gain” but actually had a loss.

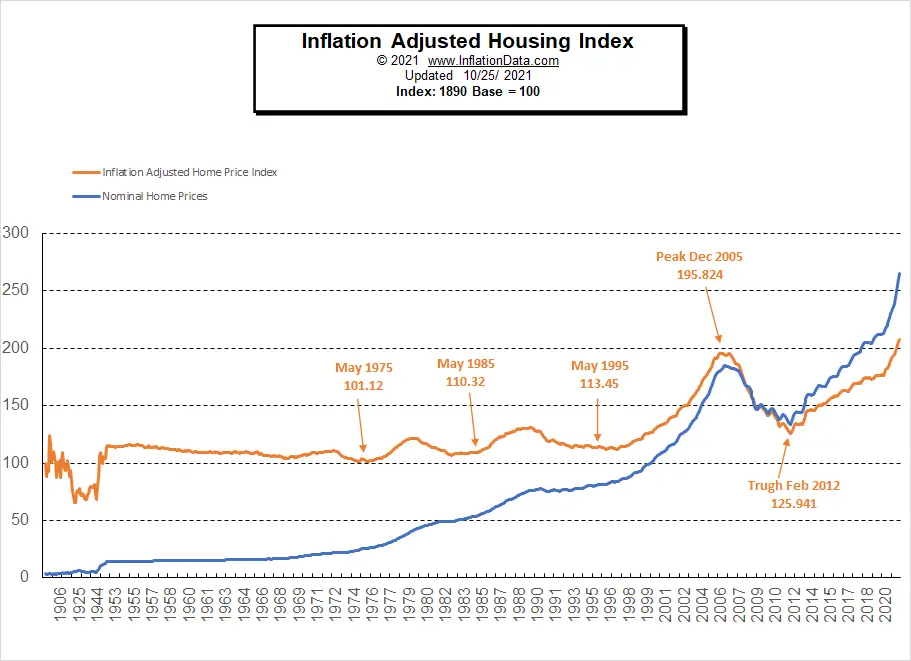

The problem is that this same logic applies to most paper-denominated assets. Assets that tend to keep up with inflation are generally commodity-based. Often things like oil, housing, and gold perform the best during periods of inflation. But even they may not fully keep up. Recently housing prices have greatly exceeded inflation, as we can see in our article on Inflation-Adjusted Housing prices. So, housing prices may fall or level off and therefore not keep up with inflation. So this time around, housing may not be the best hedge against inflation.

Hedging Against Inflation

Hedging Against Inflation

So perhaps it is best to back up a bit before trying to profit from inflation. First, we should attempt not to lose purchasing power. This is often referred to as “hedging against inflation”. The easiest way to hedge against inflation is to simply “stock up”. By that, I mean, if you will have to buy stuff anyway, why not buy it now before the price goes up? If your choice is to spend $107.50 next year or $100 now, why not just buy it now? If you put the $100 in the bank and get 1/2% interest minus taxes and then have to spend $107.50 next year, you would be better off buying it now.

So what should you buy? Once again, any commodity that you will need within the next year would be a good candidate, as long as it stores well, and you have a safe place to store it. This could be canned pantry items, toilet paper, paper towels, detergent, etc. Unfortunately, gasoline doesn’t store well, is dangerous, and takes a lot of space to store, so gasoline wouldn’t be a good storage candidate.

It is interesting to note that as more people begin to buy stuff “sooner rather than later,” it increases the “velocity of money” and creates a self-fulfilling “positive feedback loop,” which tends to increase the inflation rate. And once you consume it you will need to buy more at the higher price. But you will have eliminated at least one price increase for yourself.

Investing During Inflation

Investing in anything denominated in a fixed number of dollars will probably be a losing game. As we saw, a bank account will probably buy less next year than the value of what you put in this year. The same goes for “money market funds” and “certificates of deposit (CDs)” that earn a fixed yield. Bonds are just IOUs in a set number of dollars, so once again, unless you can buy them at a steep discount, you will probably end up losing money. The one exception is Inflation-Indexed Bonds. Basically, the government will adjust how much they pay you based on the inflation rate, but even then, with taxes and the skimpy adjustment the government pays, you will probably be lucky to break even.

Some people claim that the stock market is a good place to profit from inflation. But that depends. During periods of high inflation, companies may not be able to increase their prices enough to cover increased salaries and rising materials costs. Hence, their margins erode, their profits disappear, and their stock price declines (or doesn’t keep up with inflation). Companies like airlines might suffer from increased fuel prices and decreased passenger traffic (as people cut back on travel), so they may be especially hard-hit. On the other hand, oil producers and gold miners might benefit from higher prices. So not all stocks will increase during times of inflation, but some might.

So What Do You Do to Protect Against Inflation?

The first thing is to try to lock in as many prices at current levels as you can. For instance, if you have a lease, try to get as long a lease as possible locked it at the current price. Can you take out a mortgage at a low-interest rate? That way, you will be paying off the house with cheaper dollars, and hopefully, the house will increase in value at the rate of inflation (but as we saw, that may not be the case this time around). Maybe you can find a good deal or improve the house through renovation. Stockpile stuff that you will keep, and you will use. Watch for sales and be as frugal as possible this is not a time to waste money even though it is rapidly depreciating.

You might also like:

- Inflation-Indexed Bonds (aka i-Bonds)

- Inflation-Adjusted Housing prices

- What is the velocity of money?

Leave a Reply