Could the U.S. become the next Greece? Nope, our nightmare will be different from Greece’s. But investors will take it on the chin if they don’t take action now to protect their savings.

Greek Prime Minister George Papandreou last week blamed his country’s economic woes on credit default swap speculators. Is he kidding? Or is this just a classic red herring designed to divert attention from the real issue? It’s hard to take anyone seriously when their presidential guard dresses up like this:

I mean what’s with the poufy sleeves, the tights, and the clown shoes?

Now that I’ve offended everyone of Greek descent, I have to acknowledge that the outfits no doubt have something to do with tradition.

But whatever happened to the tradition of living within your means? That notion seems to be as quaint as the guards’ kilts.

Of course, Greece is hardly alone in its fiscal transgressions. But its revised deficit is estimated to be 12.7% of GDP. (The Greek government has admitted that previous estimates were too low.) Last week, Athens announced $4.8 billion in austerity measures – which, predictably, brought on numerous paralyzing strikes. New bonds have been issued. And though the situation is far from resolved, many say the worst is over.

The rules in the Euro zone are simple. Nobody runs a deficit of more than 3% of GDP. Nice rule. Unfortunately, there’s no enforcement mechanism. So almost everybody cheats. Check out the deficits as a percentage of GDP for a few selected countries:

|

Country |

Deficit % of GDP |

|

Iceland |

15.7% |

|

Greece |

12.7% |

|

Britain |

12.6 |

|

Ireland |

12.2% |

|

Spain |

11.4% |

|

U.S. |

10.6% |

|

Portugal |

9.3% |

|

Poland |

7.5% |

|

Italy |

5.3% |

|

Canada |

4.8% |

|

Germany |

3.3% |

No, it’s not a pretty picture. It speaks volumes about the financial dislocation happening worldwide. And notice where the U.S. is ranked. In 2010, our deficit of $1.46 trillion puts us at 10.6% of GDP. Right between Spain and Portugal. Pretty good company, huh?

Foreign central banks held $2.9 trillion in U.S Treasury obligations at the end of last year. That’s a 13-fold increase since 1999.

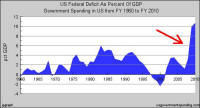

It’s not unreasonable to think that a bit further down the road our creditors’ appetite for our debt may not be as great as our need. And our need has been growing, as you can see in this chart:

If our creditors get cold feet, the game is over. Just like it would be for Greece if other countries stopped buying their debt.

But we have a secret weapon that Greece doesn’t have.

End Game

There’s really only one way out of this hole. And that’s to devalue the U.S. dollar. An outright devaluation is unlikely. Inflation is the scenario to bank on.

Greece doesn’t run the euro-money printing machine. But the U.S. prints its own dollars, and we can put our printing machine in overdrive anytime we want to.

That would enable the U.S. to pay off its debts in cheaper dollars. And many governments really don’t mind a bit of inflation. That’s because inflation helps anyone who owes money. Everyone else is a loser. Unless they’ve inflation-proofed their portfolio.

Inflation Fighters

When confidence in paper money wanes, people gravitate toward tangible assets. Michael Masterson’s art collection will do just fine when inflation rises.

What? You don’t have an art collection? Relax. There are other alternatives.

Start by positioning 10% of your portfolio in commodities. There are a number of ETFs that will give you broad exposure to these markets.

Next, be sure at least 5% of your portfolio is in precious metals. Gold gets all the press, but at IDE we like other metals better. Some, like silver, you’ve heard of. Others, like cerium and praseodymium, you probably haven’t heard of. They’re “rare earths.” We’ve mentioned them to you before. A big shortage is developing. We’ll be talking more about how you can invest in this sector.

Bonds? Wall Street gets this category all wrong. They should be about 10% of your portfolio... depending on your investment time horizon. But stay away from Government Bonds and long maturities. Think short term. And look for special-situation corporate bonds. The type Steve McDonald uncovers in his Bond Trader service.

At least 5% of your portfolio should be exposed to real estate, not counting the house you live in. There are a number of REITs that can give you this exposure. Don’t overlook rental properties. But you need to be careful here. Housing hasn’t found a bottom yet, but there are great values out there.

When it comes to stocks, favor those with growing dividends. Historically, these have held up better when inflation comes a callin’. And, with a devalued dollar, companies able to expand their overseas sales will do particularly well.

This investment news is brought to you by Investor’s Daily Edge. Investor’s Daily Edge is a free daily investment newsletter that is delivered by email before the market opens. It’s published by Fourth Avenue Financial, a subsidiary of Early To Rise (an affiliate company of Agora Publishing). In each weekday issue you’ll receive practical strategies for protecting your portfolio and multiplying your money. You’ll also learn about undiscovered opportunities in emerging sectors and markets, deeply discounted stocks, recommendations for bonds, cash, commodity and real estate investing, and top ETFs. To view archives or subscribe, visit Investor's Daily Edge.

Use our custom search to find more articles like this

Share Your Thoughts