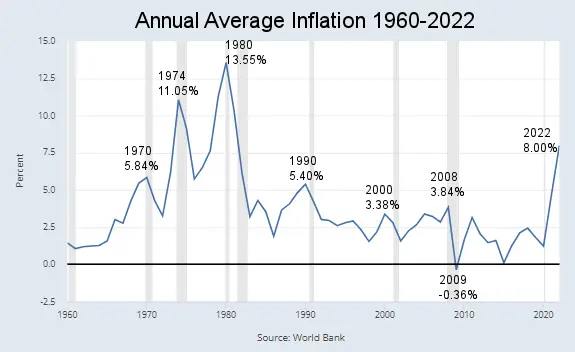

Just like the old joke, “How do you eat an elephant? …one bite at a time”, inflation is constantly “eating” away at your purchasing power. Some years your purchasing power might decline by 1%, and other years, it might decline by 5% or even 10%. As we can see from the chart above, back in 1980, purchasing power declined by an average of 13.55% over the whole year.

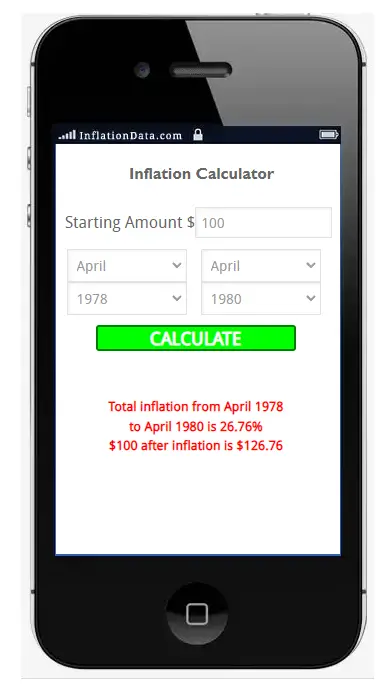

But from April 1979 to April 1980, prices increased (and thus purchasing power declined) by a whopping 14.76%. And that was on top of 10.09% from April 1978 to April 1979. So, in just two years, from April 1978 to April 1980, prices increased significantly. How much?

Well, due to compounding, you can’t simply add 14.76% and 10.09%. So, let’s look at our inflation calculator:

From the Inflation Calculator, we can see that from April 1978- April 1980 inflation increase a whopping 26.76% so something that cost $100 in 1978 would cost $126.76 two years later.

What about Merchants and Businesses?

Typically when we think about inflation, we think of increasing “Consumer Prices,” but inflation doesn’t just affect consumers. Inflation also affects producers, distributors, and merchants. Although we’d like to think that since they are big companies, they can just absorb price increases, but they can’t do that for long and still stay in business. Businesses of all sizes have expenses related to input materials and what is generally referred to as overhead.

Overhead includes everything from salaries to Office equipment and supplies, rent, depreciation, utilities, bank fees & interest, and even relatively minor things like credit card processing fees. While things like credit card processing fees might be small for a manufacturer, they can be a significant portion of expenses for companies like online retailers.

Inflation, Banking Rates, and Credit Card Processing Fees

Just like a restaurant tip is calculated based on the total bill, typically, credit card processing fees are a percentage of the total amount processed. But a lot of small transactions will cost the business a higher percentage than fewer large transactions, even if the total transaction volume is the same. This is because credit card processors charge a “transaction fee” in addition to the percentage fee.

So, although inflation typically won’t affect the percent charged, the transaction fee may increase. The total fee will increase because of the increase in the underlying totals charged. For instance, if the typical order was $100 last year and the credit card fee was 5%, the average order would incur a $5.00 processing fee plus a transaction fee. But if inflation raises the average transaction to $110, now the credit card processing fee is $5.50 plus the transaction fee. While an extra 50¢ doesn’t sound like much, it can add up for a company that does thousands of transactions a week.

Managing Inflated Credit Card Processing Fees

The idea behind mitigating inflated credit card processing fees is simple enough at its core. Merchants need to be careful about what they are paying, how much they are paying, and for what. Once they gain a thorough understanding of the fees that they are paying at any given time, they automatically gain the power to compare their current expenses with that of what the alternative options in the market have to offer. In other words, in times of high inflation, businesses need to be more vigilant about keeping costs down, which means constantly shopping around for the best deal on everything from office copy paper, to fuel, to credit card processing.

Many merchants are unaware that there are now merchant service providers that can help small businesses pass their credit card processing fees onto their customers and enjoy free credit card processing. A 0% credit card processing fee pretty much throws the inflated cost of credit card payment processing out of the equation.

In addition to processing fees and transaction fees, the typical car transaction also includes a small “interchange fee”.

Inflation and Interchange Rates

The interchange rate is basically an insurance fee collected by the merchant services provider but ultimately paid to the bank or credit card company that issued the credit card used to complete that transaction. Interchange fees are charged on a “per swipe” basis for both credit and debit cards. But since the risk to the bank is lower on debit cards, the fee for processing a debit card is generally lower than for processing a credit card.

While interchange fees are not directly correlated with inflation, they can increase when the risk of default increases. So in times of high inflation, when more consumers are defaulting on their debts, the interchange fees can increase accordingly.

So, even in areas where you wouldn’t expect inflation to have much impact, it can be one more nibble into overall cost increases, and the higher the inflation rate, the bigger the bite.

You might also like:

- How Businesses Cope With Inflation

- How Can Inflation Affect Businesses?

- Managing Business During Periods of Inflation

- What is the Phillips Curve?

- Could a Raise in Minimum Wage Trigger Inflation?

Leave a Reply