What is the Money Multiplier?

In a fractional reserve system like we have here in the United States, money is loaned out by banks and by law they are only required to have a fraction of the amount they loan out. For example, they might be required to keep 10% in reserves. In other words, they may have $10 million dollars in deposits but because not everyone will come in to claim their dollars at once the bank may loan out $9 million dollars. But the multiplication doesn’t end there. The $9 million will be deposited at another bank and that bank can loan out 90% of that or $8.1 million. And that will be deposited in another bank, who can loan out another 90% and so on.

In our article, How Wealth Can Simply Evaporate Bob Stokes gives the following example: “…a lender starts with a million dollars and the borrower starts with zero. Upon extending the loan, the borrower possesses the million dollars, yet the lender feels that he still owns the million dollars that he lent out. If anyone asks the lender what he is worth, he says, ‘a million dollars,’ and shows the note to prove it. Because of this conviction, there is, in the minds of the debtor and the creditor combined, two million dollars worth of value where before there was only one.” This is the perfect example of how the money multiplier works.

The central bank (FED) can adjust the reserve requirement to tighten or loosen the money supply. In other words, they can change the rules from requiring banks to hold 20% of their money to only 10% or up to 30% depending on their desires for the economy. When inflation is raging, the central bank will often raise reserve requirements in an effort to reduce the money multiplier.

Results of Fractional Reserve Requirements on the Money Multiplier

As you can see from the reserve requirement chart as the reserve requirement decreases the multiplier effect increases. If banks are required to maintain a 50% reserve the money virtually doubles after all the fractions are added together. At 30% the total deposits in all the banks more than triples and at 10% reserve requirements the money multiplies more than 9 times, i.e. $100 becomes over $900 after 26 individual deposits.

Is the Money Multiplier Constant?

Even if the FED maintains a constant reserve requirement the money multiplier itself can change. As a matter of fact, it is constantly changing based on a variety of market factors. The primary factor is the bank’s perception of risk. In normal situations the simple fact that there is federal deposit insurance makes the banks less risk averse, after all they can always fall back on the government.

But, if banks feel that a lot of people may come in and request their money, it might cause a “run on the bank” so they have to reduce their lending in order to have enough cash on hand to avoid that. This will reduce the money multiplier.

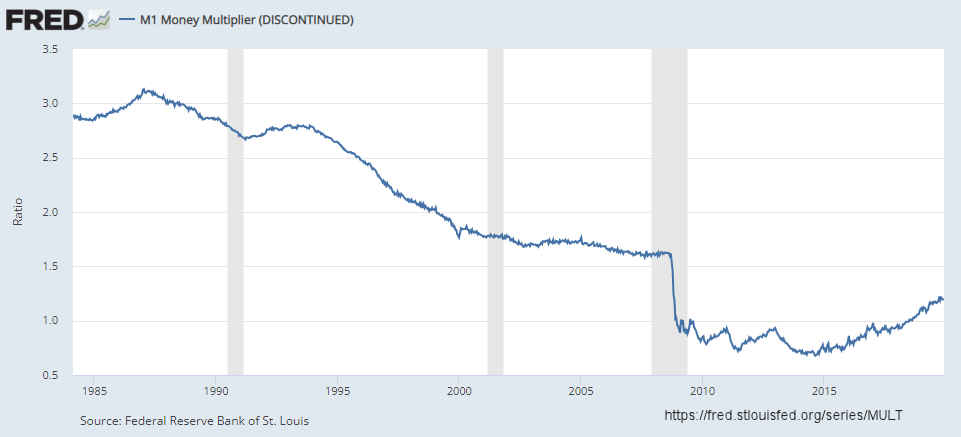

Source: https://fred.stlouisfed.org/series/MULT

Money Multiplier Chart

In the M1 Money multiplier chart, we can see that in the period from 1985 to 2011, the money multiplier ranged from above 3 to 1 down to below 1 to 1, with a drastic drop corresponding to the 2008 liquidity crisis. And in spite of massive doses of liquidity in the form of Quantitative Easing (QE1 & QE2), the money multiplier continued to stay below 1 to 1. Beginning around 2016, the money multiplier began rising again. Unfortunately, the FED discontinued publishing the money multiplier in December 2019.

Contrary to the statement of Fed Chairman Ben Bernanke who claimed that the FED could simply drop cash from helicopters to reinflate the economy…back in 1948, Nobel Prize-winning economist Paul Samuelson said,

By increasing the volume of their government securities and loans and by lowering Member Bank legal reserve requirements, the Reserve Banks can encourage an increase in the supply of money and bank deposits. They can encourage but, without taking drastic action, they cannot compel. For in the middle of a deep depression just when we want Reserve policy to be most effective, the Member Banks are likely to be timid about buying new investments or making loans. If the Reserve authorities buy government bonds in the open market and thereby swell bank reserves, the banks will not put these funds to work but will simply hold reserves. Result no 5 for 1, “no nothing,” simply a substitution on the bank’s balance sheet of idle cash for old government bonds.

And that is precisely what happened, as banks’ desire for safety increased, they refused to loan funds out except to the most worthy borrowers, and thus rather than multiply the money supply, the banks are loaning less than they are holding in their vaults. No matter how much the FED would like to encourage banks to lend, they might choose not to but instead choose to shore up their own failing balance sheets. This effect is called “pushing on a string” the FED can’t pull the banks into lending. They can only feed them the credit and hope they use it.

This same situation occurred during the great depression. Some commentators claimed that this was a sign of the greed of the bankers and their desire to foreclose on the poor farmers. But as we can see in the wake of 2008, it is mere survival instinct. The banks are not rushing to foreclose because they can’t sell the houses even if they do foreclose. But they do not want to loan more and find out that they have another worthless house on their hands either. So the bankers are trying to preserve their jobs by being extremely cautious and not risking any of the bank’s money unless they are absolutely sure it will be repaid.

Another factor is a borrower’s appetite for loans. When times are tough and you can’t handle the debt you currently have, few people want more debt, so even if rates are low, fewer applicants apply for the money.

This results in a contraction of the money supply as the money multiplier decreases and works the same as if the FED had raised the reserve requirement. In effect, the banks have raised the reserve requirement themselves in order to be sure that they remain solvent. In April 2010 I wrote an article explaining how this can result in deflation called Velocity of Money and Money Multiplier – Why Deflation Is Possible.

You might also like:

- What is Velocity of Money?

- What is Quantitative Easing?

- What is the Real Definition of Inflation?

- What is the Phillips Curve?

Leave a Reply