T here is a meme circulating around Facebook right now about Democrats voting against the 2.8% Cost of living increase. Normally, here at inflationData we try to avoid politics unless it directly relates to inflation, or our other major topics covered. But in this case I feel compelled to address this issue.

here is a meme circulating around Facebook right now about Democrats voting against the 2.8% Cost of living increase. Normally, here at inflationData we try to avoid politics unless it directly relates to inflation, or our other major topics covered. But in this case I feel compelled to address this issue.

The quick answer is that this is “NOT TRUE”. However, if the MEME was phrased slightly differently it would be “TECHNICALLY TRUE”.

If the Meme said, “NONE of the Democrats voted FOR the Social Security Cost of Living Increase” it would be “TECHNICALLY TRUE”. Likewise, if it said “NONE of the Republicans voted FOR the Social Security Cost of Living Increase” it would also be “TECHNICALLY TRUE”. That is because according to the Social Security Administration cost of living increases are automatic so they are not subject to a vote at all. And it has been automatic since 1975, prior to that Congress did have to approve them every year.

Here is what the Social Security Administration says about the COLA:

“Congress enacted the COLA provision as part of the 1972 Social Security Amendments, and automatic annual COLAs began in 1975. Before that, benefits were increased only when Congress enacted special legislation. Beginning in 1975, Social Security started automatic annual cost-of-living allowances. The change was enacted by legislation that ties COLAs to the annual increase in the Consumer Price Index (CPI-W).”

It may surprise you to know that you have Nixon to thank for the automatic Social Security increases. The 1972 landmark Social Security legislation began in 1969 when then President Richard Nixon sent Congress his recommendations for new Social Security legislation. He recommended a 10% immediate across-the-board increase in social security cash benefits. He also recommended automatic adjustments of Social Security benefits tied to future increases in the Consumer Price Index, plus he recommended other benefits increases. However, it wasn’t until 1972 that the bill was passed by Congress and it didn’t take effect until 1975.

History of Social Security COLA’s

- July 1975 — 8.0%

- July 1976 — 6.4%

- July 1977 — 5.9%

- July 1978 — 6.5%

- July 1979 — 9.9%

- July 1980 — 14.3%

- July 1981 — 11.2%

- July 1982 — 7.4%

- January 1984 — 3.5%

- January 1985 — 3.5%

- January 1986 — 3.1%

- January 1987 — 1.3%

- January 1988 — 4.2%

- January 1989 — 4.0%

- January 1990 — 4.7%

- January 1991 — 5.4%

- January 1992 — 3.7%

- January 1993 — 3.0%

- January 1994 — 2.6%

- January 1995 — 2.8%

- January 1996 — 2.6%

- January 1997 — 2.9%

- January 1998 — 2.1%

- January 1999 — 1.3%

- January 2000 — 2.5% (1)

- January 2001 — 3.5%

- January 2002 — 2.6%

- January 2003 — 1.4%

- January 2004 — 2.1%

- January 2005 — 2.7%

- January 2006 — 4.1%

- January 2007 — 3.3%

- January 2008 — 2.3%

- January 2009 — 5.8%

- January 2010 — 0.0%

- January 2011 — 0.0%

- January 2012 — 3.6%

- January 2013 — 1.7%

- January 2014 — 1.5%

- January 2015 — 1.7%

- January 2016 — 0.0%

- January 2017 — 0.3%

- January 2018 — 2.0%

- January 2019 — 2.8%

- January 2020– 1.6%

- January 2021– 1.3%

- January 2022– 5.9%

- January 2023– 8.7%

Note:

The COLA for December 1999 was originally determined as 2.4 percent based on CPIs published by the Bureau of Labor Statistics. Pursuant to Public Law 106-554,however, this COLA is effectively now 2.5 percent.

Interestingly, the increase in Social Security benefits is tied to the CPI-W rather than the more common CPI-U.

What is the CPI-W?

According to the U.S. Bureau of Labor Statistics, “The

CPI-U is a more general index and seeks to track retail prices as they affect all urban consumers. It encompasses about 87 percent of the United States’ population. The CPI-W is a more specialized index and seeks to track retail prices as they affect urban hourly wage earners and clerical workers. It encompasses about 32 percent of the United States’ population and is a subset of the CPI-U group. The CPI-W places a slightly higher weight on food, apparel, transportation, and other goods and services. It places a slightly lower weight on housing, medical care, and recreation.”

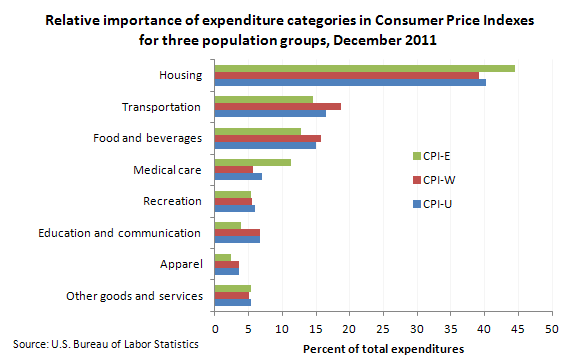

In other words, theoretically the CPI-W is a better representation of the expenses the workers who collect Social Security might expect. However, the Bureau of Labor Statistics has developed an “experimental” index called the CPI-E or Consumer Price Index for the Elderly which would probably be a better index to use for Social Security. The major difference between all three of these indexes is the weighting given to each of the various categories. For instance the elderly probably spend much less of their income on education and more on medical care than would your average Urban Consumer. Interestingly, the CPI-W actually has a lower percentage allocated toward Medical Care than the CPI-U making it LESS appropriate for Seniors than the CPI-U. It also has a Higher allocation for transportation than the CPI-U. Looking at the chart below we can see that by comparing CPI-E to the CPI-W and the CPI-U in almost every case the CPI-U would be closer to what the Elderly would actually spend than the CPI-W.

How Does the CPI-W Compare to the CPI-U?

For most years from 1980 through 1998, the CPI-W was lower than the CPI-U thus UNDERCOMPENSATING Social Security recipients. To make matters worse according to a 2007 report by the Bureau of Labor Statistics “Over the 25 years from December 1982 to December 2007, the experimental consumer price index for Americans 62 years of age and older (CPI-E) rose somewhat faster than the CPI-U and the CPI-W, mainly because prices for medical care and shelter, which are weighted more heavily in the CPI-E, increased more rapidly than overall inflation during the period.” In other words not only is the CPI-W worse than the CPI-U but the CPI-U is worse than the expenses that a typical elderly person would experience.

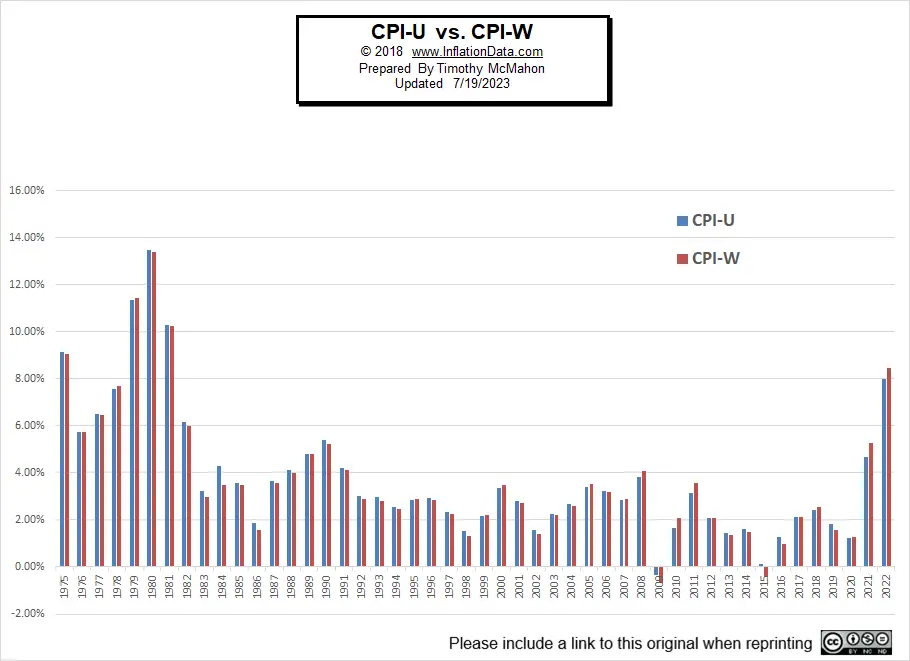

In the Chart below comparing the CPI-U and the CPI-W since 1975, we can see that although the CPI-U and the CPI-W are close they are different.

In the following table we can see the difference between the CPI-U and the CPI-W rounded to two decimal places. We can see that in the 42 years from 1975 through 2017 the CPI-U has been higher 32 times. In looking at the table we need to remember that the CPI-U and CPI-W are the values at year end and the Cola is based on the Annual CPI-W determined at the end of the third quarter of the previous year (basically 3 months in advance of the January start date). This is easy to see for 1978 for instance where the COLA was 6.5% which is the rounded value for the 1977 CPI-W. Other instances are not so obvious how they came up with the result. But sometimes 3 months can make a big difference in the annual inflation rate. Note that we do not yet have the annual inflation rate for 2018 or 2019 thus the NA. But the CPI-W at the end of the 3rd quarter was 2.8% so we know what the COLA for 2019 will be. The BLS did not start calculating CPI-E until 1983. The Social Security website did not list the COLA for 1983 (we have contacted them for clarification).

| Year | CPI-U | CPI-W | CPI-E | COLA |

| 1975 | 9.13% | 9.07% | NA | 8.0% |

| 1976 | 5.76% | 5.73% | NA | 6.4% |

| 1977 | 6.50% | 6.47% | NA | 5.9% |

| 1978 | 7.59% | 7.72% | NA | 6.5% |

| 1979 | 11.35% | 11.43% | NA | 9.9% |

| 1980 | 13.50% | 13.41% | NA | 14.3% |

| 1981 | 10.32% | 10.25% | NA | 11.2% |

| 1982 | 6.16% | 6.02% | NA | 7.4% |

| 1983 | 3.21% | 2.99% | 3.7% | NA |

| 1984 | 4.32% | 3.51% | 4.1% | 3.5% |

| 1985 | 3.56% | 3.48% | 4.1% | 3.5% |

| 1986 | 1.86% | 1.59% | 1.8% | 3.1% |

| 1987 | 3.65% | 3.59% | 4.5% | 1.3% |

| 1988 | 4.14% | 4.00% | 4.5% | 4.2% |

| 1989 | 4.82% | 4.79% | 5.2% | 4.0% |

| 1990 | 5.40% | 5.22% | 6.6% | 4.7% |

| 1991 | 4.21% | 4.11% | 3.4% | 5.4% |

| 1992 | 3.01% | 2.90% | 3.0% | 3.7% |

| 1993 | 2.99% | 2.82% | 3.1% | 3.0% |

| 1994 | 2.56% | 2.46% | 2.7% | 2.6% |

| 1995 | 2.83% | 2.88% | 2.8% | 2.8% |

| 1996 | 2.92% | 2.87% | 3.4% | 2.6% |

| 1997 | 2.34% | 2.27% | 1.8% | 2.9% |

| 1998 | 1.55% | 1.33% | 1.9% | 2.1% |

| 1999 | 2.19% | 2.19% | 2.8% | 1.3% |

| 2000 | 3.38% | 3.49% | 3.6% | 2.5% |

| 2001 | 2.83% | 2.72% | 1.9% | 2.6% |

| 2002 | 1.59% | 1.38% | 2.6% | 2.6% |

| 2003 | 2.27% | 2.22% | 2.1% | 1.4% |

| 2004 | 2.68% | 2.61% | 3.4% | 2.1% |

| 2005 | 3.39% | 3.52% | 3.6% | 2.7% |

| 2006 | 3.24% | 3.19% | 2.7% | 4.1% |

| 2007 | 2.85% | 2.88% | 4.0% | 3.3% |

| 2008 | 3.85% | 4.09% | 0.5% | 2.3% |

| 2009 | -0.34% | -0.67% | 2.2% | 5.8% |

| 2010 | 1.64% | 2.07% | 1.4% | 0.0% |

| 2011 | 3.16% | 3.56% | 2.8% | 0.0% |

| 2012 | 2.07% | 2.10% | 1.8% | 3.6% |

| 2013 | 1.47% | 1.37% | 1.6% | 1.7% |

| 2014 | 1.62% | 1.50% | 1.3% | 1.5% |

| 2015 | 0.12% | -0.41% | 1.0% | 1.7% |

| 2016 | 1.26% | 0.98% | 2.3% | 0.0% |

| 2017 | 2.13% | 2.13% | 2.2% | 0.3% |

| 2018 | 2.44% | 2.55% | 2.0% | 2.0% |

| 2019 | 1.81% | 1.59% | 2.4% | 2.8% |

| 2020 | 1.24% | 1.29% | 1.4% | 1.6% |

| 2021 | 4.69% | 5.26% | 6.4% | 1.3% |

| 2022 | 8.01% | 8.46% | 6.7% | 5.9% |

Because of the massive impact of healthcare we can see that even in years like 2016 when the CPI-U was only 1.26% and the CPI-W was only 0.98% the CPI-E was still 2.3% but Social Security only got a 0.3% increase meaning that Seniors lost 2% of their purchasing power in a single year. The previous year they saw no COLA increase but their cost of living based on the CPI-E increased by 1%. So in just those two years seniors standard of living decreased by 3%.

Since we round our data to two decimal places and the BLS rounds theirs to one, it is possible that in some instances the difference in the CPI-U and the CPI-W will be rounded out to make them equal. So in this table, we see the data rounded to a single decimal place. Whenever the data is in Red Social Security recipients received less, and when it is in Black, they received more than if it was calculated using the CPI-U. In a couple of instances, they received much less than they should have (i.e. 1984 & 1986). In 2008 and 2010, however they actually received more using the CPI-W than they would have using the CPI-U. In two instances, the CPI-W was below zero, so there was no increase in the Social Security COLA.

| Year | CPI-U | CPI-W | Difference |

| 1975 | 9.1% | 9.1% | 0% |

| 1976 | 5.8% | 5.7% | -0.1% |

| 1977 | 6.5% | 6.5% | 0% |

| 1978 | 7.6% | 7.7% | 0.1% |

| 1979 | 11.3% | 11.4% | 0.1% |

| 1980 | 13.5% | 13.4% | -0.1% |

| 1981 | 10.3% | 10.3% | 0% |

| 1982 | 6.2% | 6.0% | -0.2% |

| 1983 | 3.2% | 3.0% | -0.2% |

| 1984 | 4.3% | 3.5% | -0.8% |

| 1985 | 3.6% | 3.5% | -0.1% |

| 1986 | 1.9% | 1.6% | -0.3% |

| 1987 | 3.6% | 3.6% | 0% |

| 1988 | 4.1% | 4.0% | -0.1% |

| 1989 | 4.8% | 4.8% | 0% |

| 1990 | 5.4% | 5.2% | -0.2% |

| 1991 | 4.2% | 4.1% | -0.1% |

| 1992 | 3.0% | 2.9% | -0.1% |

| 1993 | 3.0% | 2.8% | -0.2% |

| 1994 | 2.6% | 2.5% | -0.1% |

| 1995 | 2.8% | 2.9% | 0.1% |

| 1996 | 2.9% | 2.9% | 0% |

| 1997 | 2.3% | 2.3% | 0% |

| 1998 | 1.6% | 1.3% | -0.3% |

| 1999 | 2.2% | 2.2% | 0% |

| 2000 | 3.4% | 3.5% | 0.1% |

| 2001 | 2.8% | 2.7% | -0.1% |

| 2002 | 1.6% | 1.4% | -0.2% |

| 2003 | 2.3% | 2.2% | -0.1% |

| 2004 | 2.7% | 2.6% | -0.1% |

| 2005 | 3.4% | 3.5% | 0.1% |

| 2006 | 3.2% | 3.2% | 0% |

| 2007 | 2.9% | 2.9% | 0% |

| 2008 | 3.8% | 4.1% | 0.3% |

| 2009 | -0.3% | -0.7% | No Increase in SS |

| 2010 | 1.6% | 2.1% | 0.5% |

| 2011 | 3.2% | 3.6% | 0.2% |

| 2012 | 2.1% | 2.1% | 0% |

| 2013 | 1.5% | 1.4% | -0.1% |

| 2014 | 1.6% | 1.5% | -0.1% |

| 2015 | 0.1% | -0.4% | No Increase in SS |

| 2016 | 1.3% | 1.0% | -0.3% |

| 2017 | 2.1% | 2.1% | 0% |

Under the obama administration, social security recipients did not get a cost of living increase for 8 years so don’t hand me this crap.