The 1930’s had massive deflation on a world-wide scale. Making it the worst deflationary event in living memory. This has affected the thinking and even the language of everyone from economists, to politicians, to the media, as new words like devaluation, disinflation, low inflation, even negative inflation are created to avoid having to say what they really mean and that is the big “D”… DEFLATION.

But no matter how you say it, the fact is, deflationary forces are building around the world. During the first quarter of 2015 the U.S. saw slight deflation on an annual basis. And despite historically low interest rates and high economic stimulus, in September 2015 the Financial Times posted the following telling comment:

Japan has fallen back into deflation for the first time since April 2013 in a symbolic blow to prime minister Shinzo Abe’s economic stimulus programme.

In October 2015, CNBC published an article entitled, The U.S. is Closer to Deflation Than You Think, saying deflation talk these days is mostly centered on the euro zone and parts of emerging markets, but the U.S. is dancing on the brink itself. “All price growth in the U.S. in the past eight months came from the West,” the St. Louis Federal Reserve said in a report on geographic inflation influences. Inflation in the West has been a full percentage point above the other three regions, all of which experienced deflation.

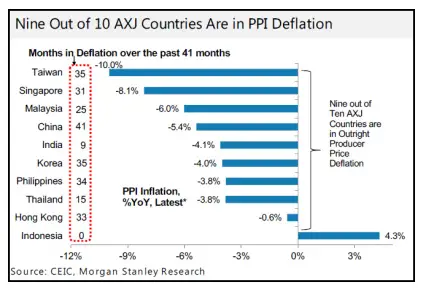

In the chart above we see Producer Price Indexes (PPI) falling in 9 out of 10 Asian countries.

So we are seeing deflationary forces in 3/4 of the U.S., in the EuroZone, in Japan, and in China and most of Asia, so deflation is still a very real force on the horizon. In the following three-part article Elliott Wave Financial Forecast looks at Devaluation, Falling Prices and the big “D” … Deflation. And unlike fighting inflation, fighting deflation is like “pushing on a string” since you can’t force people to buy or borrow, you can only encourage them through low interest rates and “easy money”. ~ Tim McMahon, editor

The Devaluation Derby

One by one, financial markets, economic measures and other critical elements of our long-term outlook for deflation and depression are falling into place. Various countries’ efforts to devalue their own currencies is a good example of the specificity of our forecast. The devaluation derby has been steadily gaining speed since March 2013, when EWFF stated, “Another clear parallel to the end of the bull market in 1929 is a sudden, global drive toward currency devaluation.” In December, we reiterated that this new trend was a “key component of our long-term forecast for monetary chaos. Still, to our chagrin, there is one main holdout: U.S. blue-chip stock indexes.”

What a difference a few weeks can make. On August 11, when China “unexpectedly devalued the yuan,” it sent “shockwaves around the world.” To us, the event was not unexpected, and we were not shocked, as noted previously. In addition to knowing the role that devaluation plays in the deflation drama, the “shockwave” of its recognition reinforces our understanding of where we are in the process. EWFF has continually stated that deflation will become widely recognized once the bear market in stocks is underway.

Leave a Reply