On August 10th 2018, the U.S. Bureau of Labor Statistics released their monthly Consumer Price Index report on the status of Inflation for the 12 months through the end of July.

Annual Inflation is Up Very Slightly

- Annual inflation in July was 2.95% up slightly from 2.87% in June. (BLS rounds both to 2.9%)

- CPI was 252.006 in July and 251.989 in June.

- Monthly Inflation for July was 0.01%, and 0.16% in June compared to -0.07% in July 2017.

- Next release September 13th

Monthly Inflation:

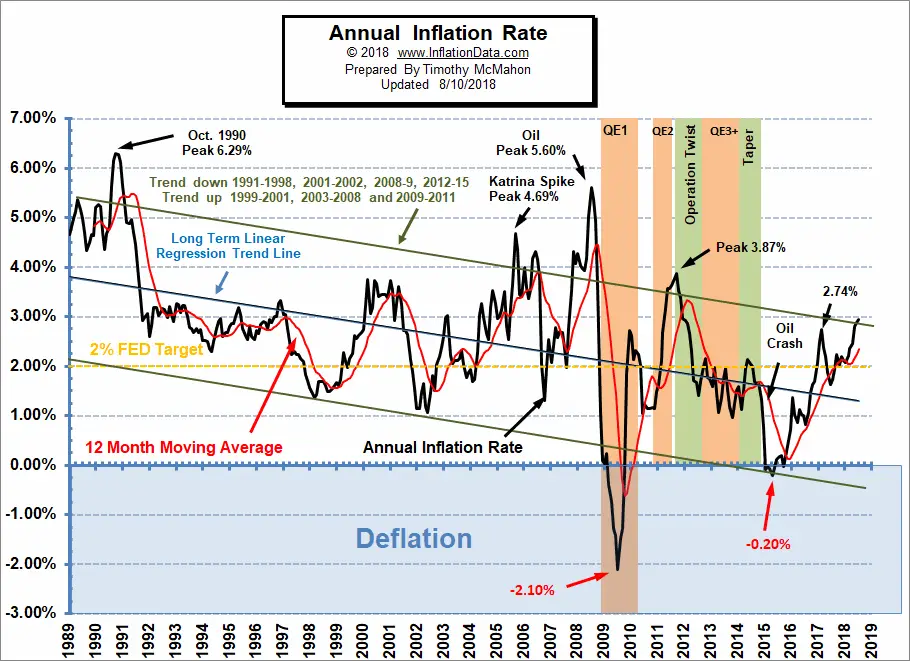

Annual inflation for the 12 months ending in July was 2.95% up from 2.87% in June. The U.S. Bureau of Labor Statistics (BLS) rounds both to 2.9% and accordingly reports the inflation rate as “unchanged”.

Since May’s annual inflation rate was 2.80% and July’s inflation rate was 2.95% there hasn’t been much change from May through July, but May was up sharply from 2.46% in April. January, February and March were 2.07%, 2.21% and 2.36% respectively each showing a progressive increase. See Annual Inflation Chart for more info.

According to the BLS commissioner’s report, “In July, the Consumer Price Index for All Urban Consumers increased 0.2 percent seasonally adjusted; rising 2.9 percent over the last 12 months, not seasonally adjusted. The index for all items less food and energy rose 0.2 percent in July (SA); up 2.4 percent over the year (NSA).”

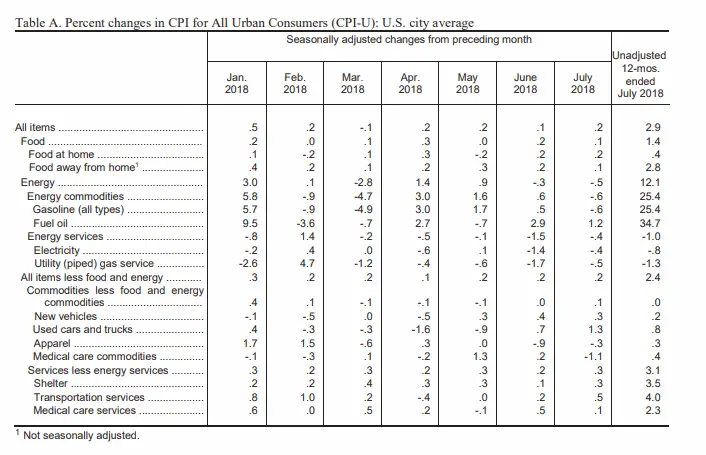

The following table shows the changes from the preceding month for the major categories in seasonally adjusted terms and for the entire 12 months in unadjusted terms.

From the table we can see that on a monthly Seasonally adjusted basis Medical Care Commodities actually fell -1.1% while fuel oil rose 1.2% but that doesn’t mean that they fully cancel each other out since they are weighted based on the percentage of an average budget that each one consumes. On an annual unadjusted basis however we see that Medical Care Commodities are up .4% and fuel oil is up 34.7%. Overall, energy is up 12.1% over the year and shelter is up 3.5%.

Typically the monthly inflation rate is highest during the first quarter (January through March) with April and May often being among the high months but not always.

The lowest monthly inflation is typically during the last quarter (October through December) with June through September typically being moderate.

Although the monthly differences seem relatively small, if we had 12 months of 0.42% inflation we would have 5.04% annual inflation but 12 months at 0.23% would only result in 2.76% annual inflation. But when higher months are combined with lower inflation months and even some negative months the annual inflation becomes much lower. So we can hope that the last quarter of this year brings the inflation rate back down. Currently our Moore Inflation Predictor is projecting that the annual inflation rate will rise above 3% over the next couple of months before falling back below toward year’s end.

Regional Inflation Information

The U.S. Bureau of Labor Statistics also produces regional data. So if you are interested in more localized inflation information you can find it here.

Food and Energy Breakdown

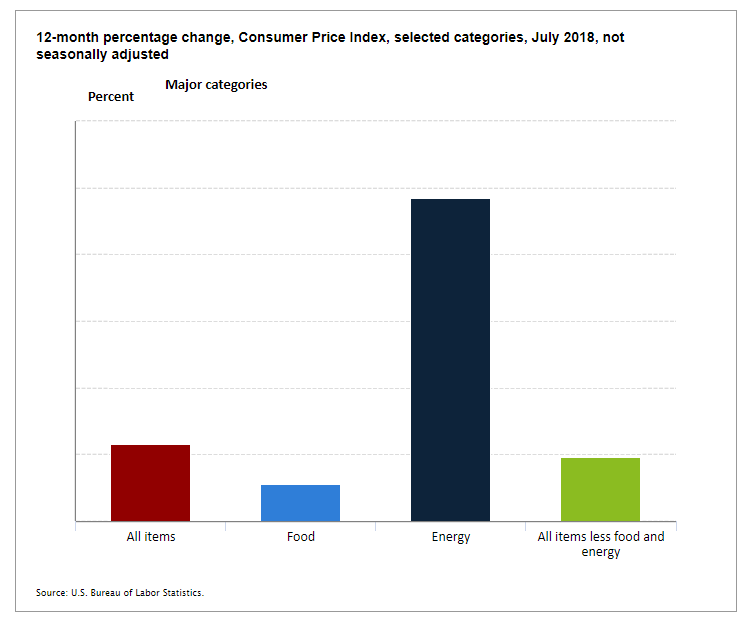

The BLS publishes an index entitled “All items Less Food and Energy” which often causes people some confusion. It doesn’t mean they stopped including food and energy in the Consumer Price Index. It just means that they have broken them out so you can compare their increase to other components. In this chart we can see the effects of food, energy and all other items on the total index. For more info see What is Core Inflation?

In the chart above it looks like energy prices should bring “All items” up more than it does. But according to the BLS energy is only 7.513% of the average household’s total budget. Food is 13.384%, Housing is 41.772%, Transportation is 16.537% etc. But you can’t simply add these percentages up either because actually energy is part of the cost of housing and also part of the cost of transportation so if you added them up you would be counting energy twice. To see the full breakdown of all the percentages go here.

In the chart above it looks like energy prices should bring “All items” up more than it does. But according to the BLS energy is only 7.513% of the average household’s total budget. Food is 13.384%, Housing is 41.772%, Transportation is 16.537% etc. But you can’t simply add these percentages up either because actually energy is part of the cost of housing and also part of the cost of transportation so if you added them up you would be counting energy twice. To see the full breakdown of all the percentages go here.

Misery Index

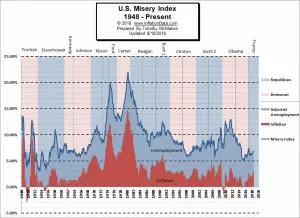

The misery index as of August 2018 (based on the most recent official government inflation and unemployment data for the 12 months ending in July)is at 6.85% down from 6.87% in June. But up from 6.60% in May and 6.36% in April. This is due to a combination of factors. At 3.90% unemployment is still below the 4.1% in March and 4.0% in June but inflation is up from 2.36% in March to 2.95% in July. This makes the misery index slightly below the 6.88% level in March 2017 but still about half of the peak of 12.87% in both October and November 2011 which was pretty miserable. The Misery index is still well below the February 2017 peak of 7.44%. The average inflation rate since the beginning of the Misery Index in January 1948 is 3.53% which is still higher than current inflation levels… so if inflation were “average” the misery index would be higher.

The misery index as of August 2018 (based on the most recent official government inflation and unemployment data for the 12 months ending in July)is at 6.85% down from 6.87% in June. But up from 6.60% in May and 6.36% in April. This is due to a combination of factors. At 3.90% unemployment is still below the 4.1% in March and 4.0% in June but inflation is up from 2.36% in March to 2.95% in July. This makes the misery index slightly below the 6.88% level in March 2017 but still about half of the peak of 12.87% in both October and November 2011 which was pretty miserable. The Misery index is still well below the February 2017 peak of 7.44%. The average inflation rate since the beginning of the Misery Index in January 1948 is 3.53% which is still higher than current inflation levels… so if inflation were “average” the misery index would be higher.

[Read More…]

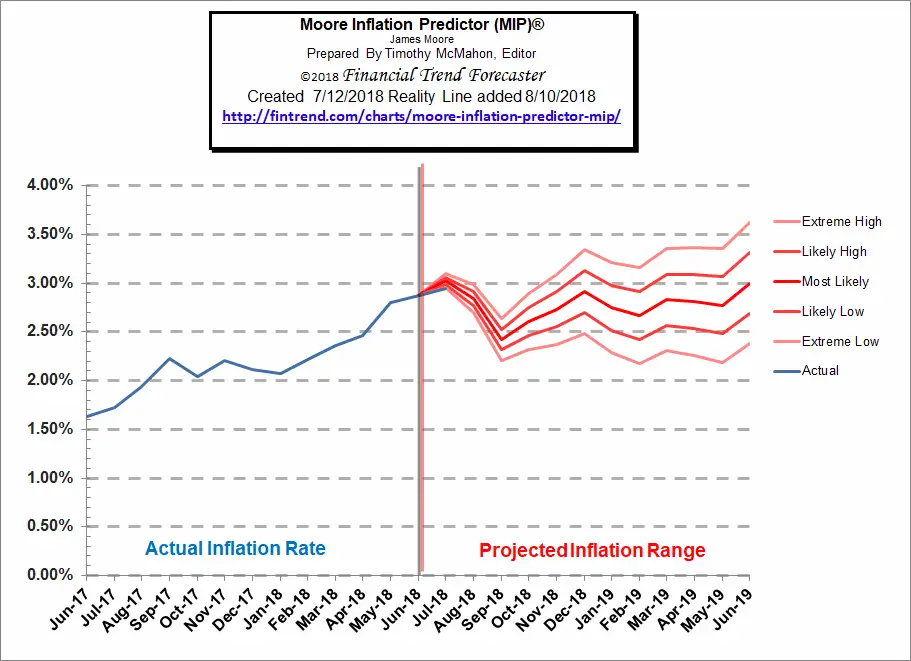

Moore Inflation Predictor

As you can see from the chart above, last month our MIP Chart was projecting a moderate increase and the actual line was right on target with our projected low (i.e. actual inflation came in on the low end of our projection).

See Moore Inflation Forecast for this month’s projection.

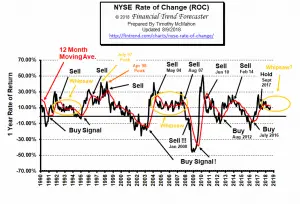

NYSE Rate of Change (ROC)©

The NYSE index has entered the “Whipsaw period” in September 2017 being above its moving average in November, below in December, above in January, below in February, back up to the moving average in March below once again in April and falling further in May and June. In July it moved further below its moving average looking very weak. However, in August we’ve seen a rebound bringing it much closer to its moving average, hinting at a crossing back above perhaps next month.

See the NYSE ROC for more info.

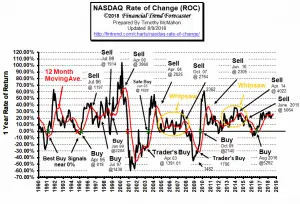

NASDAQ Rate of Change (ROC)©

The NASDAQ continues to outperform the NYSE. The annual return for the NASDAQ is 26.14% up from 24.61% last month. It was 23.14% the previous month and 20.01% the month before, so we have seen a steady increase in the annual rate of return. On the other hand, the NYSE is less than half at 10.15% up from 7.63% last month

The NASDAQ continues to outperform the NYSE. The annual return for the NASDAQ is 26.14% up from 24.61% last month. It was 23.14% the previous month and 20.01% the month before, so we have seen a steady increase in the annual rate of return. On the other hand, the NYSE is less than half at 10.15% up from 7.63% last month

See NASDAQ ROC for more.

You Might Also Like:

From InflationData.com

- What Impact (if any) Does Disruption have on Inflation?

- Debt and Inflationary Pressures: A Lesson in Economic Interactivity

- Annual Inflation Up Sharply in May

- Inflation Risk

- How Does Inflation Affect the Price of Gold?

- The Effects of Inflation and Interest Rates on Commodity Prices

Read more on UnemploymentData.com.

- Key July Employment and Unemployment Numbers

- EU Unemployment Nearing Pre-Recession Levels

- 4 Tips to Making Your Desk Job More Enjoyable

- Dress to Impress: 4 Tips to Leaving a Good Impression in a Job Interview

- Why Business Perception is Important

- Landing a Good Job Teaching ESL

- How to Know It’s Time to Start Your Own Business

- Tips for Kicking Off Your Trucking Career

- 4 Tips for Young Professionals Just Starting out

From Financial Trend Forecaster

- Why Graphene Hasn’t Taken Over the World- Yet

- New Oil Cartel Threatening OPEC

- 3 Breakthrough Technologies Changing The Energy Sector

- Can Saudi Arabia Prevent The Next Oil Shock?

- IEA: High Oil Prices “Taking A Toll” On Demand

- A New Lithium War Is About To Begin

- When Will Electric Cars Take Over The Roads?

From Elliott Wave University

- Charts Say Stocks Could Rise For 10-15 Years

- Latest Economic Data Doesn’t Align with Yield Curve Fears

- The Stock Market Big Picture

- Using Longer Timeframes To Combat Volatility Fatigue

- Recent Breakouts Say a Lot about Markets and Economy

- Are Wars Bullish or Bearish for Stocks?

- Tariffs May Not Slow Profit Momentum

- Was the 1,175 Point Drop in the DOW Unpredictable?

From OptioMoney.com

- 4 Things Home Buyers Shouldn’t Do During the Mortgage Process

- Tips for Avoiding Cash Crunches and Managing Cash Flow in Business

- How to Survive Bankruptcy

- How to Lower the Chances of Bankruptcy as a Personal Business Owner

- How to Handle Medical Bill Debt

- The Costs of Moving: 4 Thrifty Tips to Keep Your Next Move Cheap

- How Smart Entrepreneurs Manage and Insure Their Assets

From Your Family Finances

- 3 Ways Keeping Tabs on Your Credit Helps More Than Just Your Finances

- A Guide to: Making the Most of Cash Back Rewards Credit Cards

- How to Start and Build a Valuable Coin Collection

- Consistency Should Be Your Financial Foundation

- Newly Weds: 5 Reasons You Need a Financial Planner in the Early Years

- 4 Financial Planning Tips for Parents

- How to Save Money on Utilities Comfortably

- Home Office Ideas: Turn a Spare Room into Your Dream Workspace

- Diversification: The Simple Secret to Building Your Wealth

Leave a Reply