The Bureau of Labor Statistics (BLS) released their monthly Consumer Price Index (CPI-U) and Inflation report on May 22nd for the year ending in April. This resulted in the 4th month in a row where the numbers were negative (i.e. deflationary). Although the month of April itself saw prices increase 0.20% the net effect for the whole year was still -0.20%.

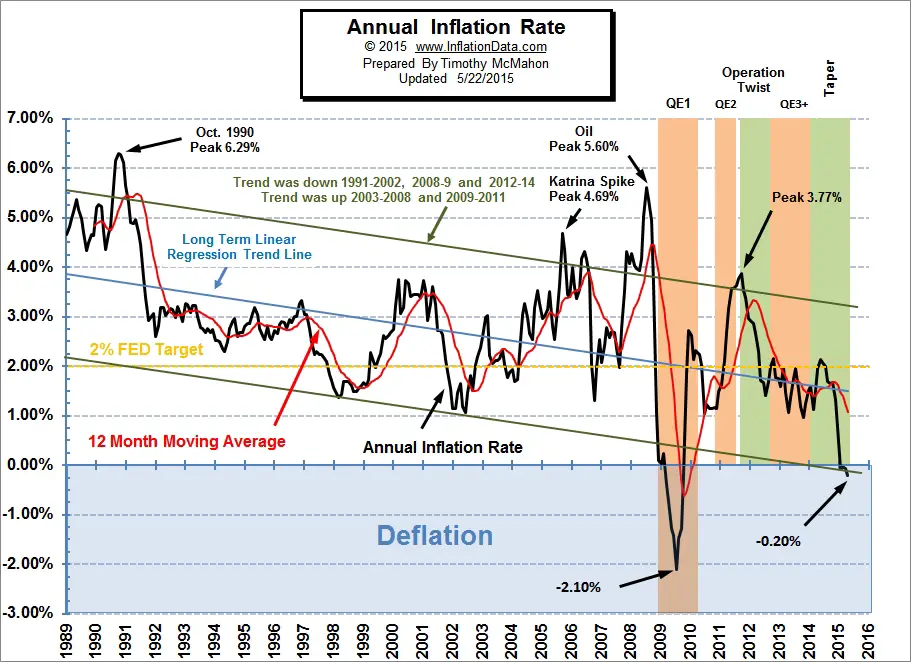

Our Annual Inflation Chart shows the downward trend in inflation since the peak in October 1990 and then the rebound after the 2008 crash due to the various quantitative easing programs. The current tapering has seen inflation fall off a cliff in 2014 with a slight deflation bias for all of 2015 so far.

Over the last month some of the key movers were Fuel Oil which fell a whopping seasonally adjusted -8.4% in the month of April and a non-adjusted -29.1% over the whole year. Natural gas fell “only” -2.6% for the month but -16.3% for the year. Food rose 2% for the year while Hospital services rose 4.8% but airfares fell -7.5%. All items less food and energy rose 1.8% and food rose 2% but that was more than offset by the -19.4% fall in energy prices.

Inflation Projections

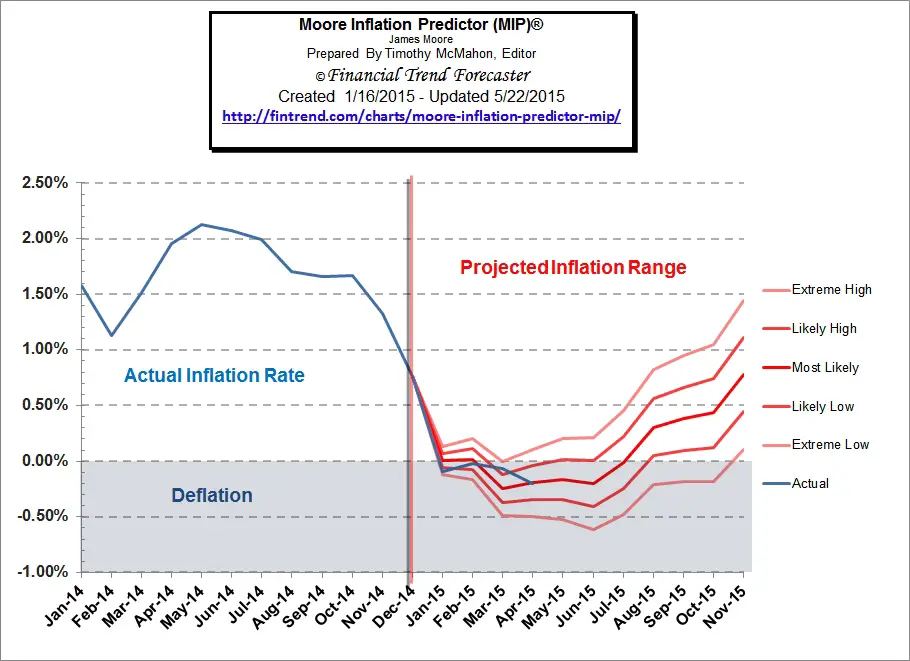

In our January Moore Inflation projection (MIP) (based on December data) we projected that inflation would drop from around 3/4% to Zero or below for the 12 month period ending in January 2015 and that is precisely what happened. We hit the nail right on the head as inflation (or should I say deflation) came in at -0.09%. (Here is the chart with the reality line added).

You can see that we were also right on target for February with the “Most likely” point virtually identical to what actually happened. March didn’t turn out quite as deflationary as we had projected but what actually happened was still well within the projection. April once again hit the “Most Likely” line right on the nose (four months in advance!)

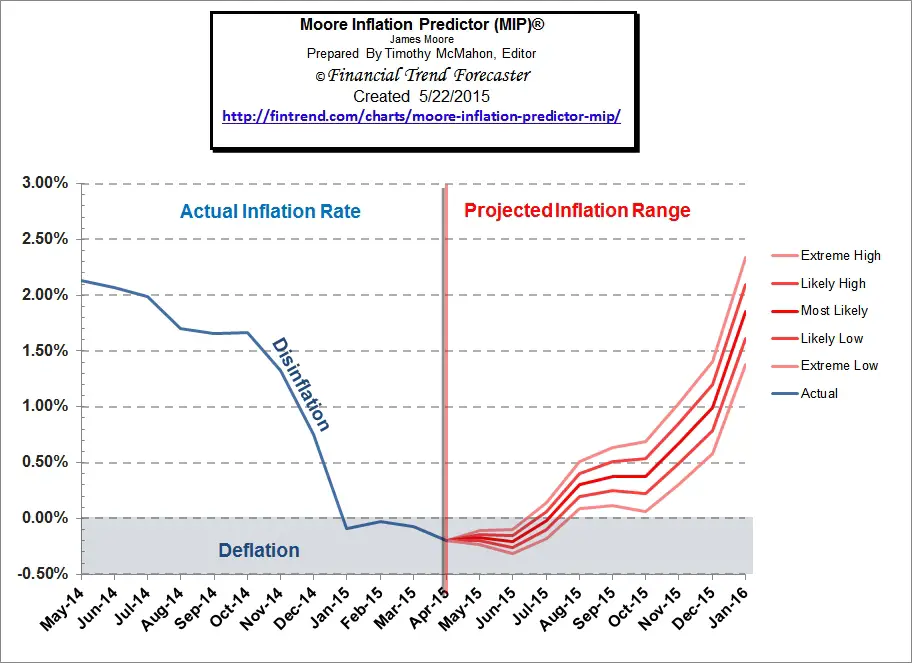

In our current MIP we are projecting a bit of ambivalence for May. It really could go either way. My guess is that it will be slightly up due to the recent run up in gasoline prices. The one interesting thing in this chart is the year end which appears to rebound sharply due to all the deflationary months from year-end 2014 falling out of the equation. But, of course, if they are replaced by equally deflationary months this year the rise won’t happen.

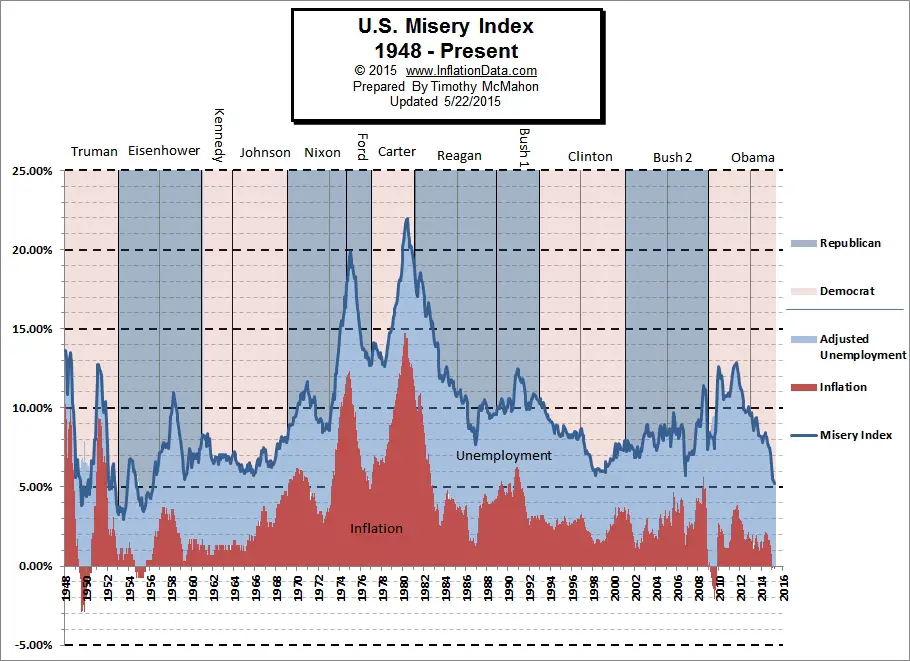

Misery Index

The misery index as of May 2015 (based on the most recent official government data for April 2015) is at 5.20% (5.4% unemployment and -0.20% inflation) down from a peak of 12.87% in both October and November 2011 which was pretty miserable.

Note: During times of deflation (i.e. negative inflation) the misery index might not be truly representative of the actual misery of the general population. Although falling prices can help alleviate suffering, deflation does not necessarily guarantee “good times” if that were the case the “Great Depression” would have to be renamed “Happy Days” since prices fell 9% in 1931 and then another 10% in 1932. See: The Great Depression The Deflationary 1930′s– 1930-1939. Even though the “Roaring 20’s” had massive deflation not everyone benefited. Those in the cities prospered but farmers suffered severely as the prices of their produce fell drastically in 1921 and 1922. See The “Roaring Twenties” Inflation and Deflation 1920-1929 .

Leave a Reply