John Maynard Keynes

Keynesian economists would have you believe that inflation is beneficial because it encourages spending which boosts demand and consequently stimulates the economy. But “Austrian” economists disagree citing the fact that inflation deludes the public into saving less than they would have normally creating malinvestment. In today’s article, we are reprinting an excellent response by Paul Vitols to a Quora question on this very topic. ~Tim McMahon, editor

Does Inflation Increase Economic Output?

By Paul Vitols

The word inflation is used by different people to point to different things. The best definition of it, in my opinion, is “a general and continuous loss of the purchasing power of money.” This is caused by steadily increasing the amount of money and credit in the economic system, a policy that is being deliberately pursued by almost all national governments in the world.

According to John Maynard Keynes, in his very influential book A General Theory of Employment, Interest and Money, published in 1936, the fundamental cause of prosperity (economic output) in society is something called “full employment,” and, again according to Keynes, the main obstacle to full employment is consumers’ tendency to save their earnings rather than spend them. Therefore, many of Keynes’s proposals involved ways to discourage people from saving their money. One such way is by adopting a policy of persistent inflation. If your money in the bank, or under your mattress, is steadily losing its value, you have an incentive to spend it now, while it’s still worth something.

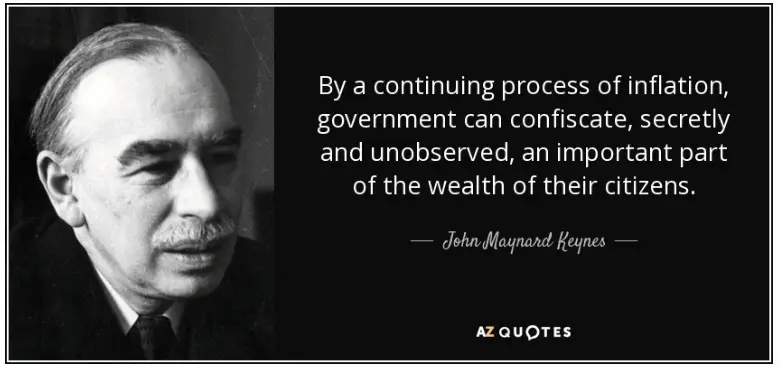

Even Keynes admitted that inflation was theft but he was in favor of it.

For my own part, I think Keynes’s ideas—certainly this one—are completely wrong. For one thing, the supposed benefits of inflation are distributed very unevenly and very unfairly. Those who are close to the source of the newly minted money and credit, such as the federal government, the banks it works with most closely, and their respective clients, enjoy a boost in wealth from receiving the newly created money while the prices in the economy still reflect the supply of money that existed before this new money was added. They are able to buy products and services at bargain prices. As that newly minted money and credit percolate through the economy, prices generally rise to reflect the increase in the money supply. By the time that new money reaches the people farthest from its source—especially low-paid people in the hinterlands—prices have already adjusted upward, but these poorer people have no power to increase their wages to compensate for the price rises. Their income is largely controlled by minimum-wage legislation, and won’t increase until government decides to raise the minimum wage. Even then, they’ll still be far behind the game. What has happened, in effect, is that wealth has been transferred from these poorest people to the richest. And this is not a one-time transfer, but a steady, ongoing drain of resources from poor to rich.

This effect was first described by the Irish-French economist Richard Cantillon, writing in the early 18th century, and is accordingly known as the Cantillon effect. Cantillon’s ideas were lost until they were rediscovered by the English economist William Stanley Jevons in the late 19th century. Although Jevons considered Cantillon’s book to be “the cradle of political economy” (according to Wikipedia), Keynes does not appear to know about him.

But there’s a still more serious problem with the policy of monetary inflation. When the value of money is systematically eroded in this way, two of money’s main reasons for existing—as a unit of account and as a store of value—are destroyed. Only its third function, as a medium of exchange, is left intact. This makes it much more difficult for businesses and entrepreneurs to make plans; now all their calculations must take into account guesses as to the future value of their currency, and they, like their workers, have to find ways to get rid of cash that is losing value, even when it might make more business sense for them to save it. Who would use the meter or the kilogram to measure things if the meter and the kilogram kept shrinking? And yet we have to use the dollar (or whatever) to measure economic value. This man-made uncertainty about the future value of money leads to mistakes in business—mistakes that are likely to be paid for more heavily by employees—workers—than by management.

Another perverse effect of inflation is that it pays businesses to try to be close to the wellhead of new money. If you can’t be an investment bank or a military contractor, you can try to be a supplier to those businesses, and thus be higher up the food chain of wealth transfer from the hinterlands. In general it does not pay as well to be providing goods and services to those hinterlands.

There are problems too with the definition of economic output. But the Cantillon effect is saying that the wealth changes of inflation are a zero-sum game. Yes, those investment banks and military contractors can engage in more business and get bigger, but the wealth is coming from hinterland workers who can afford less than they used to. Their kids get cheaper clothes and fewer Christmas presents—and we’re talking about a lot of people here.

V. I. Lenin is reported to have said that “the best way to destroy the capitalist system is to debauch the currency.” In fact, the debasing of money is a practice as old as money itself. Different regimes may rationalize it differently, but it always has the same aim: to allow rulers to spend more than they earn. To do this, they steal value from those who can’t stop them: the powerless.

I’m afraid that inflation, as a policy, is a bust. Like many bankrupt ideas, it is not even questioned by the powers that be. For them, it is a goose that keeps laying golden eggs. I believe that the pervasive, unquestioning acceptance of Keynes’s ideas in the 20th and early 21st centuries will be a puzzle for future historians.

Henry Hazlitt said it best in his 1946 book, Economics in One Lesson:

Inflation discourages all prudence and thrift. It encourages squandering, gambling, reckless waste of all kinds. It often makes it more profitable to speculate than to produce. It tears apart the whole fabric of stable economic relationships. Its inexcusable injustices drive men toward desperate remedies. It plants the seeds of fascism and communism. It leads men to demand totalitarian controls. It ends invariably in bitter disillusion and collapse.

You might also like:

Leave a Reply