The interesting thing about borrowing money long-term is that inflation actually helps you repay the loan with cheaper money… At 7% inflation, prices double roughly every 10 years, which is only 1/3rd of the way through your 30-year mortgage. So, if your budget was stretched initially to make your mortgage payment, after 10 years (assuming your salary kept up with inflation) that same mortgage would only have half the impact on your budget. Thus, to get the true impact of mortgage rates, we need to adjust them for inflation.

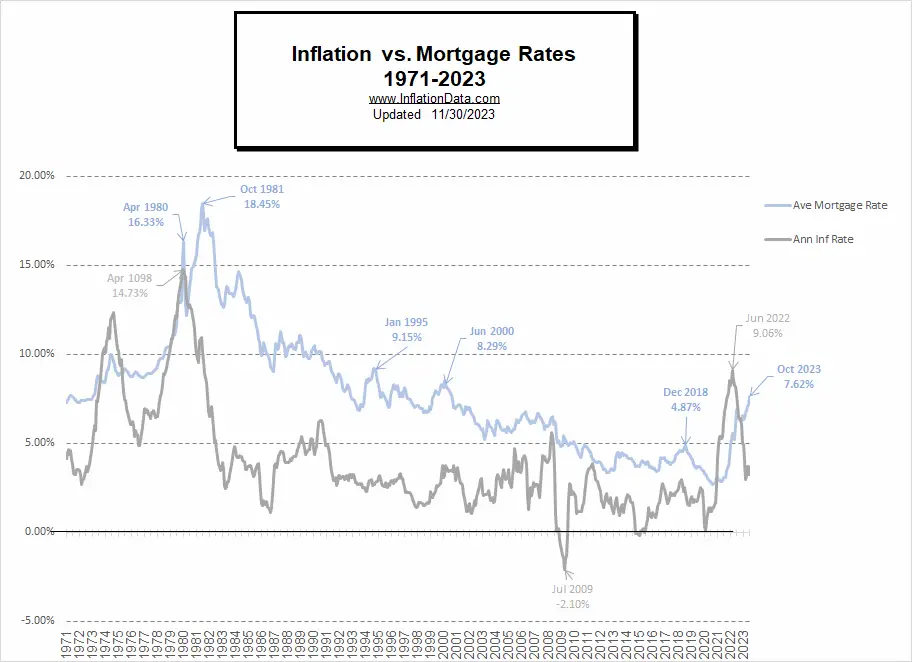

It has been a while since we addressed the issue of “Inflation Adjusted Mortgage Rates,” primarily because inflation and mortgage rates have been at historically low levels. But recently all that has changed. The COVID shutdown and massive money supply increase drove inflation up to levels not seen since the 1980s. In response, the FED raised the FED’s Funds rates. This resulted in banks raising interest rates for both borrowers and depositors. The borrowers that we are discussing today are those trying to get a mortgage. The following chart shows the average 30 year fixed mortgage rates since 1971.

Read the full article here.

Leave a Reply