From the chart below we can see that deflation was an issue in 2009 as the market eliminated billions of dollars in assets when it crashed. The FED used all the tricks in the book to combat the contraction of the money supply including lowering interest rates to near zero and when that wasn't enough it began buying assets through its "quantitative easing" (QE) programs. But the deflationary forces weren't through yet and by 2015 the FED was once again battling deflation. In the chart below we can see that after dropping interest rates to almost zero they kept them there until 2016 when they increased rates very tentatively. But in 2017 they began raising rates a bit more … [Read more...]

The Quantity Theory of Money

We have written quite extensively on the cause of inflation in articles like: How does the Money Supply affect our Inflation Rate? in What is Inflation? and Inflation Cause and Effects. One of the keys to understanding inflation is the Money Multiplier. Because of the "Fractional Reserve system banks are only required to keep a small fraction of the money on deposit as "reserves" against potential withdrawals the bank can loan out the majority of the money on deposit to earn interest. This results in a multiplication effect increasing the money supply by vast multiples. This "leverage" can work in either direction. In April 2010, I wrote an article explaining how this can result in … [Read more...]

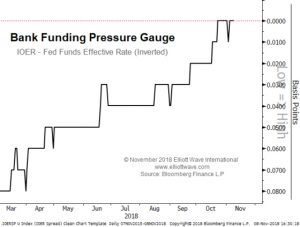

Believe Your Own Eyes: Central Banks FOLLOW the Market

Many investors believe that the market follows the FED's monetary leadership. This sounds right because the FED is the 500 pound gorilla in the market right? It has Trillions of dollars at its disposal and isn't afraid to use it. But is this actually the case? Believe Your Own Eyes: Central Banks FOLLOW the Market By Elliott Wave International 3 Videos + 8 Charts = Opportunities You Need to See. Join this free event hosted by Elliott Wave International and you'll get a clear picture of what's next in a variety of U.S. markets. After seeing these videos and charts you will be ready to jump on opportunities and sidestep risks in some major markets. This free … [Read more...]

Europe in Deflation: Got (cheap) Milk?

Why falling food prices are not a boon for Europe's economy By Elliott Wave International In the early 1990s, two simple words from a genius ad campaign radically transformed the way the U.S. consumer saw it: "Got Milk?" Suddenly, the narrative changed from an obligatory drink you had to finish as a kid, along with eating your vegetables -- into a sexy, funny, and above all desirable treat for all ages. Until now. In Europe, in 2015, famous celebrities donning milk mustaches no longer light the public's passion for lactose -- as prices for milk have spoiled. Here, a September 8, 2015 CNN Money article captures the curdled state of affairs: "So much milk is sloshing around the … [Read more...]

“Glinda the Good” Deflation Isn’t Looking So… Good

Cold weather, falling wages, bizarre fluke? The real reason consumers aren't spending is... defensive, deflationary psychology By Elliott Wave International Editor's note: You'll find the text version of the story below the video. Learn What You Need to Know NOW About Deflation Get Your Free Report Now » When 2015 began, the mainstream financial experts were certain of one thing: Even if the United States economy were sliding into deflation (which, they said, was open to discussion) that particular kind of Glinda the Good deflation, characterized by plunging energy and food prices, was going to be a boon for consumer spending: "Good deflation a tax cut for … [Read more...]

Deflation Watch: Key Economic Measures Turn South

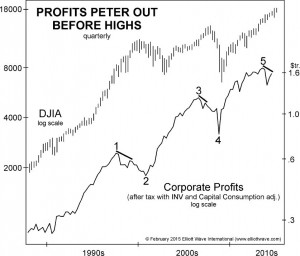

Last month (12 months ending January 2015) inflation dipped below zero resulting in an annual deflation of -0.09% rounded to -0.1% by the Bureau of Labor Statistics (BLS). The 12 months ending in February bounced up slightly to -0.03 but the BLS was able to round that up to Zero thus giving the impression that the deflation was over. But our Moore Inflation Predictor is saying otherwise. It indicates that we could be in for as much as 6 more months of deflation. And now the analysts at Elliott Wave International have found that several key economic indicators are also turning Bearish and confirming our deflation prediction. These key indicators include: Corporate profits, Retail and Food … [Read more...]

Japanese Superman Meets Economic Kryptonite

Abenomics: From Faith to Failure Why the biggest monetary stimulus effort in the world did NOT stop deflation in its tracks By Elliott Wave International When Shinzo Abe became the Prime Minister of Japan in December 2012, he was regarded with the kind of reverence that politicians dream about. He was featured in a hit pop song ("Abeno Mix"), hailed as a "samurai warrior," and featured on the May 2013 The Economist cover as none other than Superman. But in the two short years since, Abe as Superman has been struck down by the superpower-zapping force of economic kryptonite. On November 17, government reports confirmed that Japan's brief respite from a 20-year long entrenched … [Read more...]

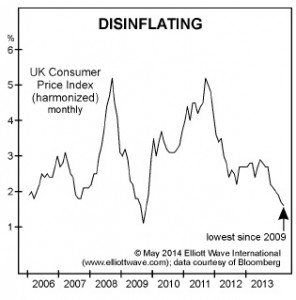

Europe is Teetering on the Edge of “Japan-Style” Deflation

Europe: The ONE Economic Comparison That Must Not Be Named... Was Just Named The Continent is now teetering on the edge of a "Japan-style" deflation. Here's our take on it. By Elliott Wave International It's happened. The one economic comparison Europe has dreaded more than any other; the name that's akin to Lord Voldemort for investors has been uttered: "deflation." And it's not just "deflation." You can still spin that term in a positive light if you get creative enough. Say, for example, "Falling prices during deflation actually encourage consumers to spend." But once you add the following two very distinct words, there's no way to turn that frown upside down. And those words … [Read more...]

Why the Fed Does Not Control Inflation and Deflation

Although we may not always agree with Steve Hochberg's conclusions the following video contains some very thought provoking ideas accompanied by some charts that you probably haven't seen anywhere else. It's interesting to note the quadrupling of the FED's leverage over the years since 2008 and the amazing lack of inflation associated with it. Check out this excellent six-minute video clip by Elliott Wave International's Steve Hochberg... at the Orlando Money Show. Despite the Fed's leverage and its attempt to inflate throughout the economy, the deflationary pressures in the U.S. are overwhelming. Gain an Advantage Over 99% of U.S. Investors - in Just 15 MinutesYou can … [Read more...]

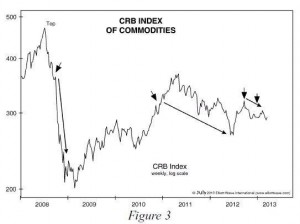

Commodity Prices Falling Despite QE

Traditional wisdom tells us that when the money supply expands the price of commodities rises. Today Robert Prechter takes a look at what has actually happened to commodity prices since 2008 during a period when theoretically the FED has been pumping up the money supply. ~Tim McMahon, editor Commodities Falling Despite QE: What Does That Mean? Robert Prechter: "Charts tell the truth. Let's look at some charts." By Elliott Wave International During QE3, the latest round of the Fed's quantitative easing, the stock market rose. We all know that. But did you also know that commodities fell? That's right: QE3 had zero effect on commodities -- or maybe even a negative effect. In … [Read more...]